Navigating the world of credit cards can be daunting, especially for new cardholders. Understanding how to avoid common credit card traps is crucial for building a strong financial foundation and maintaining a healthy credit score. This guide provides essential insights into avoiding costly mistakes and making informed decisions to maximize the benefits of your credit card while minimizing potential risks. We’ll explore key strategies for responsible credit card usage, helping you steer clear of high-interest rates, hidden fees, and other pitfalls.

Many new credit card users fall prey to enticing offers and alluring rewards programs, often overlooking the fine print. This article will equip you with the knowledge to discern beneficial credit card features from potentially harmful ones. Learn how to choose the right credit card for your needs, manage your credit card debt effectively, and avoid the common traps that can lead to financial hardship. We’ll cover topics like interest rates, annual fees, late payment penalties, and strategies for responsible spending to build a positive credit history.

Intro Offers vs Real Rates

Navigating the world of credit cards as a new cardholder can be daunting, especially when confronted with the alluring promises of introductory offers. These offers, often featuring low or 0% APRs for a limited time, can seem incredibly attractive, potentially masking the less appealing real rates that follow.

It’s crucial to understand the difference. Introductory offers are temporary incentives designed to attract new customers. They typically last for a specified period, often 6, 12, or 18 months. After this period expires, the interest rate reverts to the card’s standard APR, which is the real rate you’ll be paying. This real rate can be significantly higher than the introductory rate, sometimes exceeding 20%.

Failing to recognize this distinction can lead to serious financial repercussions. If you haven’t paid off your balance before the introductory period ends, you’ll suddenly be facing a much higher interest rate, resulting in substantial interest charges. This can quickly snowball, making it difficult to manage your debt.

Therefore, before applying for a credit card, carefully examine the terms and conditions, paying close attention to the length of the introductory period and the subsequent real rate. Consider whether you can realistically pay off your balance within the introductory period. If not, the seemingly attractive introductory offer might ultimately prove to be a costly mistake.

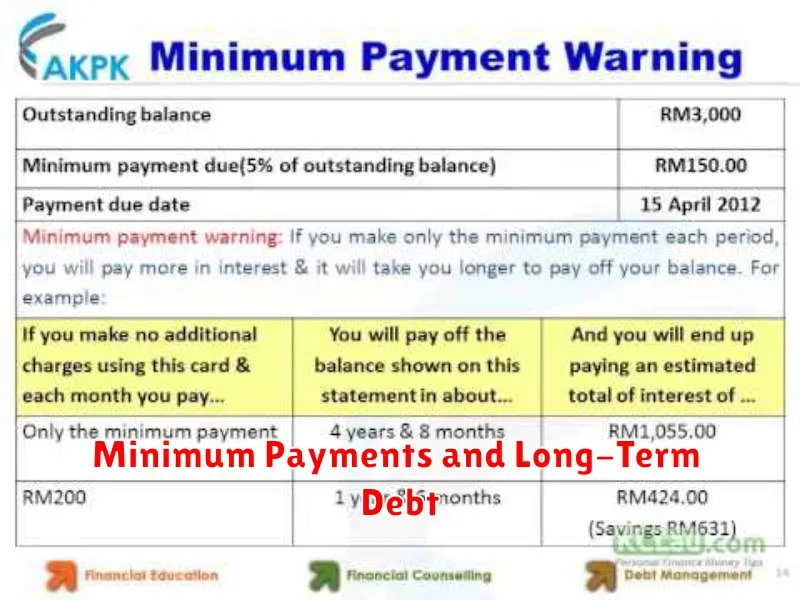

Minimum Payments and Long-Term Debt

One of the biggest traps new credit card holders fall into is the reliance on minimum payments. While seemingly convenient, consistently paying only the minimum significantly prolongs the repayment period and leads to accumulating substantial long-term debt.

The reason for this lies in the high interest rates associated with credit cards. A large portion of your minimum payment goes towards interest, leaving only a small fraction to reduce the principal balance. This means you’re essentially paying more in interest over time than you are paying down your debt.

Consider this example: Let’s say you have a balance of $1,000 with a 18% annual interest rate and a minimum payment of $25. Paying only the minimum will take significantly longer than anticipated to repay the balance. Meanwhile, the interest charges continue to accumulate, making the total cost of the purchase considerably higher.

To avoid this debt trap, make it a priority to pay more than the minimum payment each month. Even an extra $25 or $50 can drastically reduce the overall interest paid and shorten the repayment time. Creating a budget and allocating funds specifically for credit card payments can be immensely helpful.

Furthermore, understanding the terms and conditions of your credit card agreement is crucial. Knowing the interest rate, minimum payment calculation, and any associated fees will equip you to make informed financial decisions and proactively manage your debt.

Avoiding Over-Limit and Late Fees

One of the biggest pitfalls for new credit card holders is incurring over-limit and late fees. These charges can significantly impact your credit score and overall financial health. Understanding how to avoid them is crucial for responsible credit card management.

To prevent over-limit fees, carefully track your spending against your credit limit. Many credit card companies offer online tools and mobile apps that provide real-time updates on your balance and available credit. Utilizing these resources allows you to stay informed and avoid exceeding your limit. Consider setting up spending alerts to receive notifications when you approach your limit.

Late fees are equally detrimental. The best way to avoid them is to establish a system for timely payments. Consider setting up automatic payments to ensure your payment is submitted on time, each month. Alternatively, mark your payment due date prominently on your calendar or use reminder apps to ensure you don’t miss it. Remember that even a day late can trigger a fee.

Understanding your credit card statement is vital. Familiarize yourself with the due date and the minimum payment amount. While paying the minimum payment avoids late fees, it’s generally advisable to pay more than the minimum to reduce your balance and avoid accumulating interest charges. Paying your balance in full each month is the most effective way to manage your credit card debt and avoid unnecessary fees.

Proactive credit card management is key to avoiding over-limit and late fees. By utilizing available tools, setting up payment reminders, and understanding your statement, you can build a strong credit history and avoid the financial burden of these avoidable charges.

Understanding the Billing Cycle Timeline

Understanding your credit card’s billing cycle is crucial for avoiding late payment fees and maintaining a good credit score. The billing cycle is the period of time, typically a month, between when your statement is generated and when your payment is due.

Your statement will show all transactions made during that billing cycle. The statement closing date marks the end of the billing cycle, and the date your statement is generated. It is important to note that this is not the due date.

The payment due date is usually 21-25 days after the statement closing date. This is the date by which your payment must be received by your credit card issuer to avoid late payment fees. Failing to pay by the due date will negatively impact your credit report and incur penalties.

Grace period is the time between the statement closing date and the payment due date. During this period, you can pay your balance in full to avoid paying interest. If you only make a minimum payment, interest will accrue on the remaining balance from the statement closing date.

Carefully review your statement each month. Note both the statement closing date and the payment due date. Using online banking or setting up automatic payments can help you manage your payments and avoid missing deadlines.

Paying attention to these key dates will ensure that you avoid late fees and maintain a healthy credit standing. Remember, consistently paying your balance on time is essential for building a strong credit history.

How to Track Your Spending Efficiently

Effectively tracking your spending is crucial to avoiding credit card debt. Accurate record-keeping allows you to understand your spending habits, identify areas for improvement, and stay within your budget.

There are several methods you can employ. Budgeting apps offer convenient ways to automatically categorize and track transactions. Many link directly to your bank and credit card accounts, providing a real-time overview of your finances. Popular options include Mint, Personal Capital, and YNAB (You Need A Budget).

Alternatively, a spreadsheet or notebook provides a more manual approach. You can meticulously record each transaction, categorizing expenses (e.g., groceries, transportation, entertainment). This method demands more discipline, but offers a high degree of customization.

Regardless of your chosen method, consistent recording is key. Aim to log your transactions daily or at least weekly. The more frequently you update your records, the more accurate and insightful your financial picture will be. Delaying tracking increases the likelihood of overlooking expenses and misjudging your spending.

Finally, regularly review your spending data. Analyze your spending categories to pinpoint areas where you might be overspending. This analysis will help you make informed decisions about adjusting your budget and developing more responsible spending habits.

Establishing Healthy Card Habits Early

Developing healthy credit card habits from the start is crucial for long-term financial well-being. Many young adults are eager to obtain their first credit card, viewing it as a symbol of independence. However, without proper guidance and understanding, this can quickly lead to financial difficulties. It’s essential to approach credit card ownership with responsibility and a clear understanding of its implications.

One of the most important steps is to choose a card wisely. Consider cards designed for beginners with lower credit limits and fewer fees. This minimizes the potential for high debt accumulation. Avoid cards with high interest rates, hefty annual fees, or complicated reward programs that can be easily misunderstood. Understanding the terms and conditions is paramount before accepting any card offer.

Budgeting is key to responsible credit card usage. Before making any purchases, carefully assess your income and expenses to ensure you can comfortably afford to repay the balance in full each month. Tracking spending habits using a budgeting app or spreadsheet can help you stay on track and avoid overspending. This diligent approach helps build a strong credit history.

Paying your credit card bills on time and in full is perhaps the single most important habit to cultivate. Late payments negatively impact your credit score, which can have significant consequences for future financial endeavors such as securing a loan or renting an apartment. Setting up automatic payments can help ensure that your payments are always made promptly.

Finally, regularly monitoring your credit report is a vital aspect of maintaining healthy credit card habits. This enables you to identify any errors or discrepancies and take the necessary steps to correct them. It allows you to track your progress and ensure your credit score reflects responsible financial behavior. Consistent attention to these factors will build a foundation for strong financial health.

{kind=link}