Securing a business loan can be a pivotal moment for any entrepreneur, offering the financial boost needed for expansion, innovation, or weathering economic storms. However, the landscape of business financing is fraught with potential pitfalls. Navigating the complexities of loan offers requires vigilance, as seemingly attractive opportunities can conceal significant risks. This article will equip you with the knowledge to identify business loan red flags, empowering you to make informed decisions and avoid costly mistakes. We’ll explore crucial indicators that signal a risky offer, helping you protect your business finances and future.

Understanding the characteristics of a risky business loan is critical for preserving your company’s financial health. From hidden fees and exorbitant interest rates to predatory lending practices and opaque terms, numerous deceptive strategies can trap unsuspecting borrowers. By learning to recognize these red flags, you can proactively safeguard your small business loan application process and ultimately select a reliable lender that offers fair and transparent terms. This will ultimately lead to better financial outcomes and sustainable growth for your venture. This guide is designed to help you confidently assess loan offers and make smart financial choices.

Unclear Terms or Unexplained Fees

One of the most significant red flags in a business loan offer is the presence of unclear terms or unexplained fees. A reputable lender will be transparent about all aspects of the loan agreement, ensuring you understand every cost involved before signing.

Look out for contracts containing vague language or clauses that are difficult to interpret. This lack of clarity often hides unfavorable conditions that could negatively impact your business. Hidden fees, such as prepayment penalties, late fees, or excessive origination fees, are particularly concerning and should prompt further investigation.

Scrutinize the fine print meticulously. If you’re unsure about anything, don’t hesitate to ask for clarification. A trustworthy lender will readily explain all aspects of the loan agreement in plain language, without resorting to technical jargon or evasiveness. If the lender is reluctant to answer your questions or dismisses your concerns, it’s a serious warning sign.

Be especially wary of loans that promise extremely favorable terms without fully disclosing the costs involved. Such offers may be too good to be true, potentially masking predatory lending practices. Transparency is paramount; anything less should be considered a major red flag.

Before committing to any business loan, ensure you have a complete understanding of all fees, interest rates, repayment schedules, and other relevant terms. If aspects remain unclear or unexplained, it’s best to walk away and explore alternative financing options.

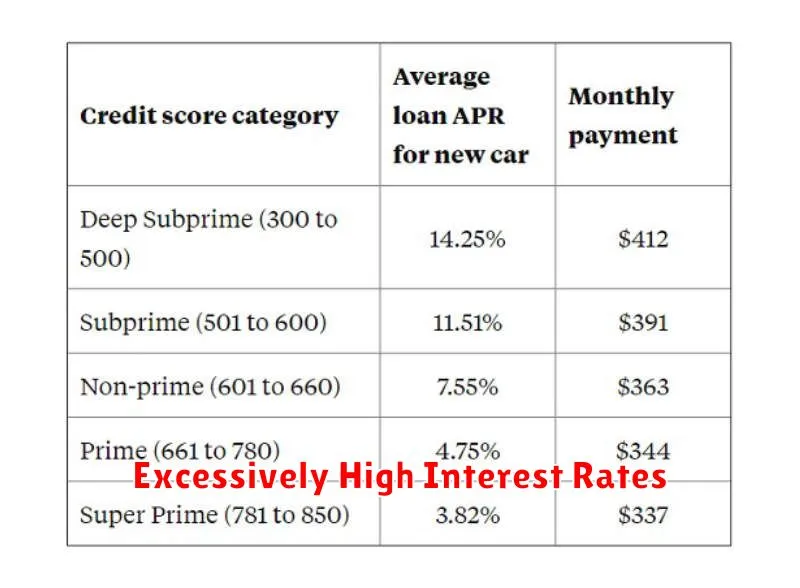

Excessively High Interest Rates

One of the most glaring red flags in a business loan offer is an excessively high interest rate. While interest rates fluctuate based on market conditions and the borrower’s creditworthiness, an unusually high rate should immediately raise concerns.

Compare offers from multiple lenders. This allows you to gauge the competitive market rate for loans with similar terms and your credit profile. A significantly higher rate compared to the average suggests the lender may be exploiting your financial needs.

Consider the overall cost of borrowing. The interest rate is only one component. Scrutinize all associated fees, including origination fees, prepayment penalties, and any other charges. These can significantly increase the total cost of the loan, even if the interest rate appears initially reasonable.

Understand the reasons behind a high interest rate. A lender may justify a higher rate due to perceived higher risk, such as a weak business plan or insufficient collateral. However, be wary of lenders who fail to provide a clear and transparent explanation for the elevated rate. A lack of transparency could indicate predatory lending practices.

Don’t rush into a decision. Take your time to analyze multiple offers and carefully consider the implications of a high interest rate on your business’s long-term financial health. A slightly higher rate might be acceptable if offset by other favorable terms, but an excessively high rate often points towards a risky loan.

Pressure to Decide Quickly

One of the most significant red flags when considering a business loan is the pressure to make a quick decision. Legitimate lenders understand that securing financing is a crucial decision requiring careful consideration and due diligence. They will provide you with the necessary time to review the terms and conditions, seek independent advice, and compare offers.

High-pressure sales tactics, such as limited-time offers or threats of the loan being withdrawn, are often employed by predatory lenders. These tactics aim to bypass your critical thinking process and prevent you from fully evaluating the risks involved. Be wary of any lender who pressures you to sign on the dotted line without adequate time for review.

A legitimate lender will be happy to answer your questions and address your concerns, providing you with all the necessary information to make an informed decision. They will not rush you into a commitment, understanding that a well-considered choice is far more valuable than a hasty one. If you feel pressured to decide quickly, it’s a strong indicator that the offer might be too good to be true, and likely carries significant risk.

Remember, taking your time to analyze the loan terms, fees, and repayment schedule is essential. Don’t let aggressive sales tactics compromise your ability to assess the true cost and potential pitfalls of the loan. Your financial health depends on it.

No Review of Financials or Plan

One of the most glaring red flags in a business loan application process is the complete absence of a review of your financials and business plan. Legitimate lenders require a thorough understanding of your financial situation and future projections to assess the risk involved. This involves scrutinizing your income statements, balance sheets, cash flow statements, and your business plan itself.

Without this assessment, the lender is essentially operating blindly. They can’t accurately determine your ability to repay the loan, making it a high-risk venture for you, even if the terms seem attractive. A lender’s lack of interest in these key documents should raise serious concerns about their legitimacy and their commitment to responsible lending practices.

Expect questions about your revenue streams, expenses, debt levels, and your overall business strategy. A lender who doesn’t ask these questions, or dismisses them outright, is likely operating without the due diligence necessary to make an informed decision. This can indicate a predatory lending practice aimed at securing borrowers regardless of their creditworthiness or repayment ability.

The lack of scrutiny also suggests a potential lack of understanding of the business itself. A sound business plan is crucial, detailing your market analysis, competitive advantages, and financial projections. A lender overlooking this integral element highlights a significant deficiency in their evaluation process, suggesting they are prioritizing speed and ease of loan approval over responsible lending.

Short-Term Loans With Large Final Payments

One significant red flag to watch out for when considering a business loan is a short-term loan structured with an exceptionally large final payment. This type of loan, often marketed as a quick and easy solution, can create a serious financial burden for your business.

The problem lies in the disproportionate size of the final balloon payment. While the monthly or quarterly installments might seem manageable initially, the lump sum due at the end of the loan term can be unexpectedly high, potentially jeopardizing your business’s cash flow and financial stability. Failing to meet this substantial final payment can lead to severe penalties, including default and potential legal action.

Before committing to such a loan, carefully analyze your projected cash flow to ascertain your ability to handle the large final payment. Consider the potential impact on other financial obligations and whether you have sufficient reserves to cover unforeseen circumstances. Lack of planning for this significant final payment is a common cause of business failure when these types of loans are used.

Furthermore, examine the overall cost of the loan. While the initial monthly payments may appear attractive, the high final payment could inflate the total interest paid significantly, making it a less favorable option compared to other loan structures. Always compare the total cost to other loan options available.

In short, while the allure of a seemingly low initial payment on a short-term loan is tempting, the potential for a crippling final payment makes these deals risky. Proceed with extreme caution and thoroughly evaluate the terms before signing any agreements.

How to Compare Offers Safely

Comparing business loan offers requires a methodical approach to ensure you’re making a safe and informed decision. Avoid rushing the process; thoroughly review each offer before making a commitment.

Focus on the Annual Percentage Rate (APR): The APR is a crucial factor, representing the total cost of the loan, including interest and fees. Don’t just compare interest rates; a lower interest rate might be offset by higher fees, resulting in a higher APR. Carefully examine the APR of each offer to accurately compare the overall cost.

Analyze the Loan Terms: Loan terms significantly impact the total cost. Consider the loan’s repayment period (length of the loan), and how that influences your monthly payments and overall interest paid. A shorter loan term may lead to higher monthly payments but ultimately less interest paid over the life of the loan. Conversely, a longer term reduces monthly payments but increases the total interest paid.

Scrutinize Fees: Pay close attention to all associated fees, including origination fees, prepayment penalties, and late payment fees. These fees can add up substantially and significantly impact the effective cost of the loan. Compare the total fees across different offers to identify the most cost-effective option.

Understand the Lender’s Reputation: Research the lender thoroughly. Check online reviews and ratings to gauge their reputation for transparency, customer service, and adherence to lending practices. A lender with a poor reputation could signal potential issues throughout the loan process.

Verify the Lender’s Licensing and Compliance: Ensure the lender is properly licensed and compliant with all relevant state and federal regulations. This helps protect you from fraudulent lenders or those with unethical practices.

Use a Loan Comparison Tool (with Caution): While online loan comparison tools can be helpful, use them judiciously. Verify the information provided by the tool with the lender’s official documents to ensure accuracy. Remember, these tools often prioritize lenders that pay them for referrals, so don’t solely rely on their rankings.

{kind=link}