Are you dreaming of owning a home but unsure about the financial commitment? Understanding your potential monthly mortgage payment is a crucial first step in the home-buying process. This comprehensive guide will equip you with the knowledge and tools to accurately estimate your monthly mortgage payment, taking into consideration various factors that influence the final cost. We’ll break down the key components of a mortgage payment, allowing you to confidently navigate the complexities of home financing and make informed decisions about your future.

Accurately estimating your monthly mortgage payment is essential for budgeting and financial planning. Knowing your likely monthly mortgage payment ahead of time enables you to determine your affordability, explore different loan options, and make a realistic assessment of your financial capacity. This article will provide you with a clear understanding of how to calculate your mortgage payment, including principal, interest, property taxes, and homeowner’s insurance, offering valuable insights into the overall cost of homeownership. Learn how to use online mortgage calculators and understand the impact of interest rates on your payments.

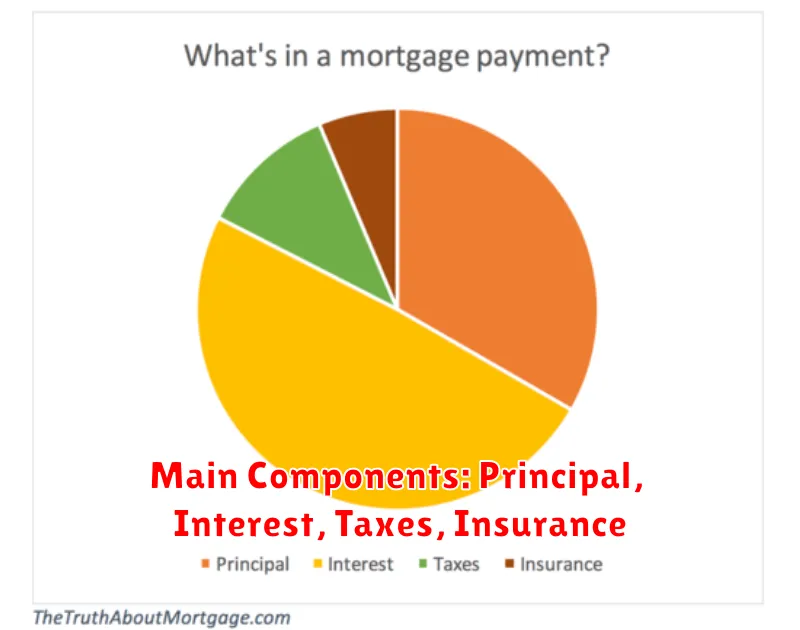

Main Components: Principal, Interest, Taxes, Insurance

Understanding the main components of your monthly mortgage payment is crucial for accurate budgeting. These four key elements – principal, interest, taxes, and insurance – combine to form your total monthly payment.

The principal is the actual amount of money you borrowed from the lender to purchase your home. Each monthly payment includes a portion that goes towards reducing this principal balance. Over the life of the loan, your principal payments gradually decrease the amount you owe.

Interest is the cost of borrowing money. It’s calculated as a percentage of your remaining principal balance. In the early stages of your mortgage, a larger portion of your payment goes towards interest, while later on, a larger portion goes towards principal. The interest rate significantly impacts your overall payment amount.

Property taxes are levied by your local government and are usually included in your monthly mortgage payment through a process called escrow. The lender collects these taxes along with your mortgage payment and pays them to the relevant authorities on your behalf. The amount you pay depends on your property’s assessed value and the local tax rate.

Homeowners insurance protects your property from damage caused by various events, such as fire, theft, or storms. Similar to property taxes, this is typically included in your monthly mortgage payment through escrow. The cost of insurance varies depending on several factors, including your home’s value, location, and coverage level.

Using Online Mortgage Calculators Effectively

Online mortgage calculators are invaluable tools for estimating your monthly mortgage payments. They provide a quick and convenient way to explore different scenarios and understand the potential financial implications of homeownership. However, it’s crucial to use them effectively to obtain accurate and helpful results.

Accuracy depends heavily on the input data. Ensure you provide the most precise information possible. This includes the loan amount, the interest rate (which can fluctuate, so use a current rate), the loan term (typically 15 or 30 years), and any applicable property taxes and homeowner’s insurance costs. Failing to input all relevant figures will yield an inaccurate estimate.

Many calculators allow you to explore the impact of down payment variations. Experimenting with different down payment amounts can show how this affects your monthly payment and overall loan cost. A larger down payment typically results in a lower monthly payment and a reduced total interest paid over the life of the loan.

Remember that online calculators provide estimates, not exact figures. Your actual monthly payment may vary slightly depending on the lender’s specific fees and closing costs. It’s always best to consult with a mortgage professional for a precise calculation and personalized advice tailored to your unique financial situation. They can account for factors not included in basic calculators, such as private mortgage insurance (PMI) if your down payment is less than 20%.

Consider using multiple online mortgage calculators to compare results and ensure consistency. Different calculators may use slightly different calculation methods, so comparing outputs can provide a better overall understanding of your potential monthly payment.

Fixed vs Adjustable Rate Estimates

When estimating your monthly mortgage payment, a crucial decision involves choosing between a fixed-rate and an adjustable-rate mortgage (ARM). Understanding the implications of each is paramount to accurate budgeting.

A fixed-rate mortgage offers predictable monthly payments throughout the loan’s term. The interest rate remains constant, providing financial stability and allowing for easier long-term budgeting. While potentially offering a higher initial interest rate compared to ARMs, the predictability minimizes financial surprises.

Conversely, an adjustable-rate mortgage features an interest rate that fluctuates over time, typically based on an underlying index like the London Interbank Offered Rate (LIBOR) or the Secured Overnight Financing Rate (SOFR). This means your monthly payment can change periodically, potentially increasing or decreasing. While an ARM might start with a lower interest rate than a fixed-rate loan, the uncertainty surrounding future payments necessitates careful consideration.

To accurately estimate your monthly payment, you need the loan amount, the interest rate (fixed or initial rate for ARMs), and the loan term. Online mortgage calculators readily provide estimates based on these inputs. Remember that for ARMs, the initial estimate represents only the first few years’ payments; after that, the rate, and therefore the payment, is subject to change.

It’s essential to obtain estimates from multiple lenders to compare rates and terms. Consider your financial risk tolerance and long-term goals when making your choice between a fixed-rate and an adjustable-rate mortgage. A financial advisor can provide personalized guidance based on your individual circumstances.

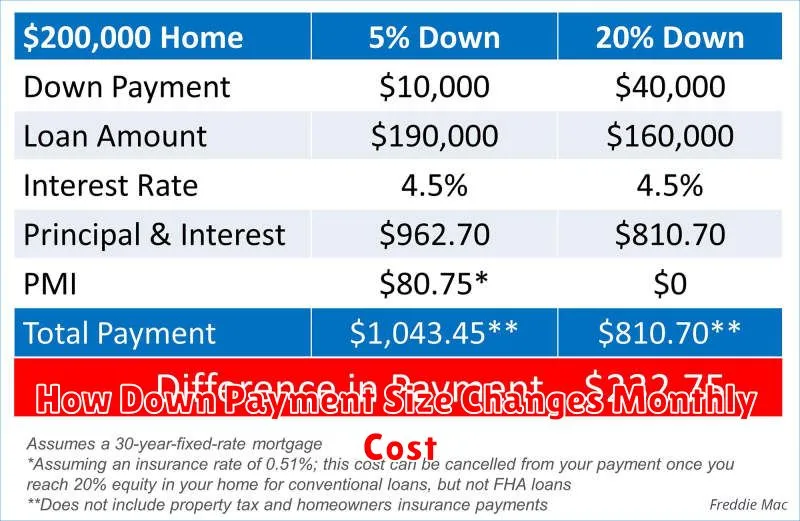

How Down Payment Size Changes Monthly Cost

The size of your down payment significantly impacts your monthly mortgage payment. A larger down payment reduces the loan amount you need to borrow. This, in turn, directly lowers your monthly principal and interest payment.

For example, let’s say you’re buying a $300,000 home. With a 20% down payment ($60,000), you’ll borrow $240,000. However, with a 10% down payment ($30,000), your loan amount increases to $270,000. The larger loan amount necessitates higher monthly payments over the life of the loan, even if the interest rate remains the same.

Furthermore, a smaller down payment often results in a higher interest rate. Lenders perceive borrowers with smaller down payments as higher risk, leading them to charge a higher rate to compensate for that perceived risk. This increased interest rate adds to the overall monthly cost, making the impact of a smaller down payment even more significant.

Private Mortgage Insurance (PMI) is another factor. If your down payment is less than 20%, lenders typically require PMI. This is an added monthly expense that protects the lender if you default on your loan. The cost of PMI varies but adds considerably to your overall monthly mortgage payment. Once you reach 20% equity in your home, you can typically request PMI cancellation, reducing your monthly payment.

In summary, a larger down payment translates to a lower loan amount, potentially a lower interest rate, and the avoidance of PMI. All of these factors contribute to a lower monthly mortgage payment. Therefore, saving for a substantial down payment is a crucial step in managing your monthly housing costs.

Factoring in HOA and Maintenance

When estimating your monthly mortgage payment, it’s crucial to consider additional costs beyond the principal, interest, taxes, and insurance (PITI) typically included in a loan estimate. These additional costs significantly impact your overall housing expense.

Homeowners Association (HOA) fees are a common expense for those living in condominiums, townhouses, or some planned communities. These fees can vary widely depending on the amenities offered, the size of the community, and its financial health. Be sure to obtain a detailed breakdown of HOA fees from the seller or HOA management company, as this is a recurring monthly cost that cannot be overlooked.

Beyond HOA fees, you also need to factor in maintenance costs. Even in communities with HOAs covering exterior maintenance, you’ll still be responsible for interior repairs and upgrades. Regular maintenance, such as appliance repairs, plumbing issues, and landscaping, can add up quickly. To accurately estimate this expense, consider the age of the property, the condition of its systems (HVAC, plumbing, electrical), and your personal maintenance habits. Building a small buffer into your budget for unexpected repairs is highly recommended.

Combining HOA fees and maintenance costs with your PITI provides a more realistic picture of your total monthly housing expense. This comprehensive figure will help you make informed decisions about your budget and affordability. Failing to account for these additional expenses can lead to financial strain and even foreclosure in the long term.

Budgeting for the Unexpected

While calculating your principal, interest, taxes, and insurance (PITI) is crucial for estimating your monthly mortgage payment, it’s equally important to budget for unexpected expenses. A realistic budget should account for potential financial hiccups that may arise.

Home repairs and maintenance are inevitable. Appliances break down, roofs need repairs, and plumbing issues occur. Factor in a monthly contingency fund dedicated to these unforeseen costs. A good rule of thumb is to allocate 1-2% of your home’s value annually for maintenance, spread evenly across your monthly budget.

Beyond maintenance, you should also consider HOA fees (if applicable) and potential special assessments. HOAs often levy special assessments for major repairs or improvements to the community, which can significantly impact your monthly budget. Inquire about the HOA’s financial history and any potential future assessments to prepare.

Furthermore, interest rate fluctuations can affect your monthly payment, especially if you have an adjustable-rate mortgage (ARM). Building a buffer into your budget to accommodate potential interest rate increases will prevent financial strain. Consider incorporating a safety net that covers a potential increase of a few percentage points.

Finally, remember to factor in property taxes. While typically included in your PITI calculation, property tax rates can change year to year. Be prepared for potential increases by including a margin of error in your monthly budgeting.

{kind=link}