Securing a business loan can be crucial for growth, but navigating the application process can be daunting. Lenders require a clear and compelling explanation of your request, demonstrating not only your need for funds but also your ability to repay. This article provides a comprehensive guide on how to effectively communicate your business loan needs to a lender, increasing your chances of approval. We’ll cover crafting a persuasive loan application, highlighting your strong financial projections, and addressing potential lender concerns proactively. Learn how to present a robust case for your small business loan or term loan, showcasing the potential for high return on investment (ROI).

Understanding what information lenders prioritize is paramount. This guide will walk you through the essential components of a successful loan proposal, including a detailed business plan, financial statements reflecting your creditworthiness, and a clear articulation of your loan purpose and repayment strategy. We’ll explore techniques for demonstrating financial stability, mitigating risk, and building a strong relationship with your potential lender, all crucial steps in securing the financing your business needs. Mastering these strategies will significantly increase your approval odds and ultimately help your business thrive.

Crafting a Clear and Specific Loan Purpose

When applying for a business loan, clearly articulating the purpose of the loan is paramount. Lenders need to understand exactly how the funds will be used to ensure the loan is a sound investment and to mitigate their risk.

Avoid vague statements like “to improve the business” or “for working capital.” Instead, provide specific details. For example, instead of “working capital,” specify “to purchase inventory for the upcoming holiday season,” or “to cover payroll expenses during a period of increased demand.” The more precise you are, the better the lender can assess the viability of your request.

Your explanation should demonstrate a direct link between the loan funds and a measurable outcome. This could be increased sales, improved efficiency, expansion into a new market, or the acquisition of key equipment. Quantify your expectations whenever possible. For instance, instead of saying “to upgrade our technology,” state “to purchase a new accounting software system that will automate our invoice processing, reducing administrative costs by 15% within six months.”

Highlighting the return on investment (ROI) for the lender is crucial. Show how the loan will generate profits and repay the debt. This might involve projecting increased revenue, cost savings, or market share gains. A well-defined and quantified plan demonstrates your understanding of the financial implications and your commitment to repaying the loan.

Remember to keep your language concise and professional. Use clear, straightforward language, avoiding jargon or overly technical terms. A well-structured and easily understandable loan purpose statement significantly increases your chances of securing the funding you need.

Linking the Loan to Business Growth Goals

A successful loan application hinges on clearly demonstrating how the requested funds will directly contribute to your business’s growth and profitability. Lenders aren’t simply interested in providing capital; they want to see a viable plan for repayment and a demonstrable return on their investment.

Therefore, meticulously linking your loan request to specific, measurable, achievable, relevant, and time-bound (SMART) goals is crucial. Instead of vaguely stating you need funds for “expansion,” articulate precisely how the loan will facilitate that expansion. For instance, will it fund the purchase of new equipment to increase production efficiency by a certain percentage? Or will it cover marketing costs for a targeted campaign aiming to boost sales by a specific amount within a defined timeframe?

Provide concrete examples of how the loan will be used. Detail the anticipated impact on key performance indicators (KPIs) such as revenue, profit margins, market share, and customer acquisition costs. Quantify the expected returns and present realistic projections supported by market research and financial forecasts. A strong business plan, including detailed financial projections, is indispensable in this process. This will illustrate your understanding of the financial implications and your commitment to responsible financial management.

Remember to highlight the long-term benefits of the loan beyond immediate gains. Will it facilitate entry into new markets? Will it allow for the development of innovative products or services? Clearly articulating the long-term vision and demonstrating how the loan is a critical component in achieving that vision is persuasive to lenders.

In short, the connection between the loan and your business’s growth aspirations needs to be crystal clear and convincingly presented. This demonstrates not only your understanding of your business but also your responsible approach to financial planning and management.

Supporting Data: Revenue, Projections, Cash Flow

Lenders require concrete financial data to assess the viability of your loan request. This isn’t simply about providing numbers; it’s about demonstrating a clear understanding of your business’s financial health and future potential. The most crucial elements are revenue, projections, and cash flow statements.

Revenue data should showcase your historical performance. Provide at least two years’ worth of financial statements, including income statements and balance sheets. This demonstrates a consistent income stream and helps the lender gauge your business’s stability. Clearly highlight key performance indicators (KPIs) such as total revenue, cost of goods sold, and gross profit margin. Be prepared to explain any significant fluctuations or trends.

Projections are arguably just as important as historical data. Lenders need to see that you’ve thoughtfully considered your business’s future. Your projections should be realistic and based on sound assumptions. Include a detailed pro forma income statement, a cash flow projection, and a balance sheet projection for at least the next three to five years. Clearly articulate the basis for your projections and any underlying market research or industry analysis you’ve conducted. Be ready to defend your assumptions.

Cash flow is a critical metric for lenders. They want to see that you can consistently generate enough cash to meet your debt obligations. Present a detailed cash flow statement, highlighting both operating, investing, and financing activities. Explain how you will manage your cash flow to ensure timely loan repayments. Address any potential cash flow shortfalls and explain your mitigation strategies.

Remember to present your financial data in a clear, concise, and professional manner. Use charts and graphs where appropriate to visually represent key data points. Ensure all figures are accurate and readily auditable. Providing well-organized and easily understandable financial documentation significantly improves your chances of securing the loan.

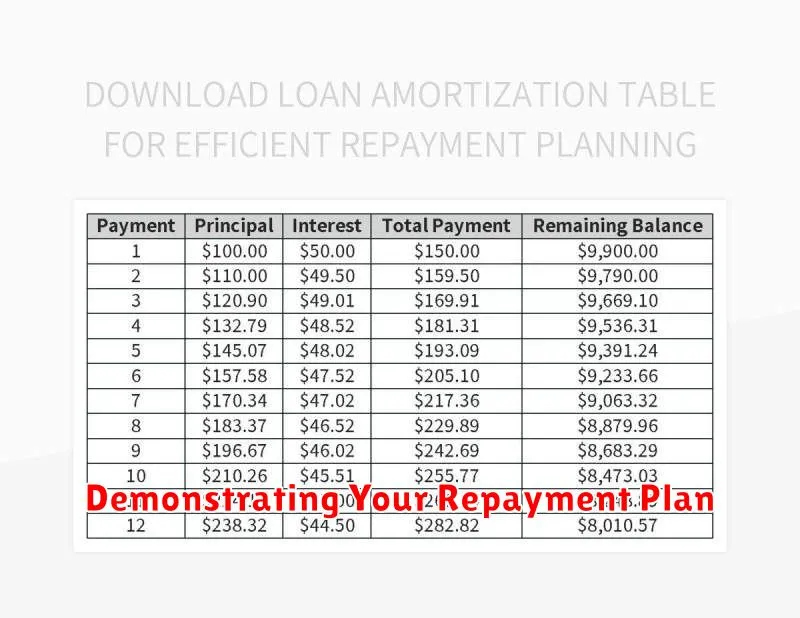

Demonstrating Your Repayment Plan

A crucial element of a successful business loan application is a clearly articulated and convincing repayment plan. Lenders need assurance that you possess the capability and strategy to repay the loan according to the agreed-upon terms. This demonstration goes beyond simply stating your intent; it requires providing concrete evidence of your financial capabilities.

Your repayment plan should detail your projected cash flow, demonstrating how your business will generate sufficient income to cover loan repayments. This often involves presenting financial projections, including income statements, cash flow statements, and balance sheets, forecasting revenue and expenses over the loan term. Realistic and conservative projections are key; overestimating income or underestimating expenses will immediately raise red flags with the lender.

Include a detailed schedule outlining the proposed monthly or quarterly loan payments. This schedule should be directly tied to your projected cash flow, illustrating how these payments fit within your overall financial picture. Be prepared to explain any periods of potentially lower cash flow and how you intend to manage those fluctuations. Highlighting any existing collateral or assets that can serve as security also strengthens your repayment plan.

Furthermore, showcasing a strong management team and a well-defined business strategy bolsters your credibility. A lender will assess the overall health and potential of your business. A sound business plan, proven market demand, and a competent team significantly increase your chances of securing the loan. Clearly demonstrating your understanding of the market, your competitive advantages, and your ability to manage risks all contribute to a compelling repayment plan.

Finally, maintain transparency and accuracy throughout your repayment plan. Lenders are experienced in detecting inconsistencies or unrealistic projections. A well-structured, realistic, and thoroughly supported repayment plan significantly increases your chances of securing the necessary financing for your business.

Addressing Risks and How You’ll Mitigate Them

Lenders are inherently risk-averse. They need to understand not only the potential for profit in your business, but also the potential for loss. Addressing these risks head-on and demonstrating a clear plan to mitigate them is crucial for securing your loan.

Begin by identifying the key risks associated with your business. These might include market competition, economic downturns, dependence on a single client or supplier, or seasonality of sales. Be thorough and honest in your assessment. Don’t try to downplay or ignore potential problems; instead, acknowledge them upfront.

For each identified risk, outline your mitigation strategy. This is where you demonstrate your preparedness and foresight. For example, if your risk is competition, you might detail your unique selling proposition, your marketing plan, and your capacity to adapt to changing market conditions. If the risk is economic downturn, you could explain your contingency plan, including cost-cutting measures and alternative revenue streams.

Specific and measurable mitigation strategies carry more weight. Instead of saying “we’ll manage risks effectively,” explain precisely what steps you’ll take: “We will maintain a cash reserve equal to three months’ operating expenses,” or “We will diversify our customer base to reduce dependence on any single client.” Use data and projections to support your claims.

Demonstrating a proactive and well-thought-out approach to risk management builds lender confidence. It shows that you’ve considered potential challenges and are prepared to navigate them successfully. This increases the likelihood of securing the loan and obtaining favorable terms.

Do’s and Don’ts During a Loan Pitch

Preparing for a loan pitch requires meticulous planning and a clear understanding of your target audience. Knowing what to do and, equally important, what to avoid can significantly impact the success of your request.

Do’s:

- Clearly articulate your business needs: Explain precisely how the loan will be used and the expected return on investment (ROI). Provide specific examples and avoid vague statements.

- Showcase your financial preparedness: Present detailed financial projections, including income statements, cash flow statements, and balance sheets. Demonstrate your understanding of your business’s financial health.

- Highlight your experience and expertise: Emphasize the skills and knowledge of your team, and showcase any relevant industry experience. This builds confidence in your ability to manage the loan and achieve your goals.

- Be prepared for questions: Anticipate potential questions from the lender and prepare thorough answers. This demonstrates your preparedness and professionalism.

- Maintain professionalism: Dress appropriately, speak clearly and concisely, and maintain a respectful and confident demeanor throughout the presentation.

- Provide a compelling narrative: Frame your business plan as a story. Connect emotionally with the lender by showcasing the passion and vision behind your enterprise.

Don’ts:

- Overestimate your potential: Avoid unrealistic projections and inflated claims. Accuracy and honesty are paramount.

- Downplay risks: Acknowledge potential challenges and present a clear strategy for mitigating those risks. Transparency builds trust.

- Be unprepared: Arriving without necessary documentation or lacking a clear understanding of your financials will severely damage your credibility.

- Overwhelm with information: Focus on the most important aspects of your business plan. Avoid overwhelming the lender with unnecessary details.

- Be defensive or argumentative: Listen attentively to feedback and answer questions calmly and professionally, even if you disagree.

- Forget to follow up: After the pitch, send a thank-you note and follow up on the lender’s feedback and timeline for a decision.

{kind=link}