Graduating college is a significant milestone, but it often comes with the daunting reality of student loan debt. Navigating the transition from student to working professional while managing loan repayments can feel overwhelming. This comprehensive guide, “How to Prepare Financially for Graduation with Student Loans,” provides practical strategies and essential tips to help you effectively manage your student loan debt and build a solid financial foundation after graduation. We’ll cover everything from understanding your loan terms and exploring repayment options to budgeting effectively and building good credit.

Effective financial planning before and after graduation is crucial for mitigating the impact of student loans. This guide will empower you to make informed decisions about your loan repayment, develop a realistic budget, and create a plan for long-term financial success. Learn how to prioritize debt repayment, explore strategies for reducing interest, and build a strong financial future despite the challenges of student loan debt. Take control of your finances and start planning for your post-graduation journey with confidence.

Know Exactly What You Owe and to Whom

Before you even think about your post-graduation plans, gain a complete understanding of your student loan debt. This involves more than just knowing the total amount. You need a precise breakdown of each individual loan.

Identify each lender. This could be the federal government (through programs like Direct Loans), a private lender, or a combination of both. Note the name of the lender, the loan’s identifier (loan number), and the type of loan (e.g., subsidized, unsubsidized, Stafford, Perkins, private).

Determine the principal balance, interest rate, and repayment terms for each loan. This information is usually available online through your lender’s website or your student loan servicer’s portal. Your servicer is the company responsible for collecting your payments. Gathering all this information is crucial for making informed decisions about repayment strategies.

Consider creating a spreadsheet or using a dedicated student loan tracking tool to organize this data. This will allow you to easily visualize your debt and track your progress as you pay it down. You’ll want to be aware of any differing interest rates and repayment schedules to prioritize your repayment efficiently.

Understanding your debt in detail empowers you to make effective repayment plans and avoid potential issues such as late payments or default. Having a clear picture of who you owe and how much is the foundation for successful post-graduation financial management.

Understand Your Grace Period

Graduating college is a significant achievement, but it also marks the beginning of student loan repayment. Before you panic about the looming debt, understand that most federal student loans offer a grace period.

This grace period is a crucial timeframe typically lasting six months after you graduate, leave school, or drop below half-time enrollment. During this period, you are not required to make any loan payments. It provides a buffer to allow you to transition into a job, adjust to your new financial responsibilities, and prepare for loan repayment.

However, it’s critical to note that interest may still accrue on your loans during the grace period. This means the principal loan amount will increase, and you’ll end up owing more than the original loan amount if you don’t actively pay down some of the interest during this time. Understanding how interest capitalization works during this period will be beneficial.

The length of the grace period can vary depending on your loan type and lender, so it’s essential to review your loan documents carefully. Contact your loan servicer if you have questions about your specific grace period. Taking proactive steps to understand this period will ensure a smoother transition into repayment.

While the grace period offers temporary relief, it’s a limited opportunity. Don’t let it become a source of future financial stress. Use this time wisely to develop a robust repayment plan, explore repayment options, and actively manage your finances to minimize the overall cost of your student loans.

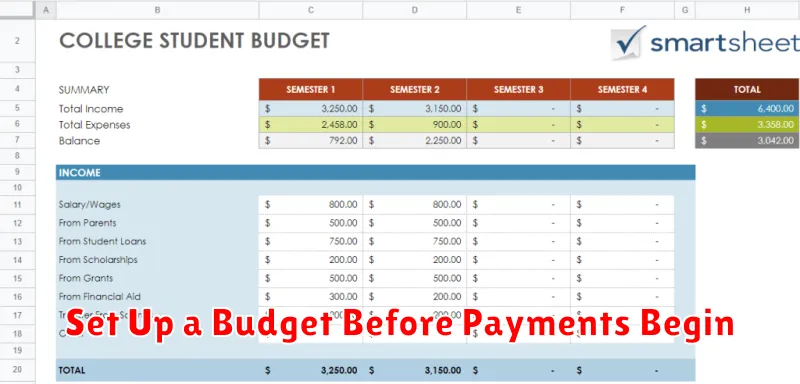

Set Up a Budget Before Payments Begin

Before your student loan payments begin, creating a detailed budget is crucial. This allows you to visualize your monthly income and expenses, ensuring you can comfortably manage your loan payments without compromising your financial stability.

Start by listing all sources of income, including your salary, part-time job earnings, or any other regular income streams. Be realistic and conservative in your estimations.

Next, meticulously track your expenses. Categorize them into essential needs (housing, utilities, groceries, transportation) and discretionary spending (entertainment, dining out, subscriptions). Use budgeting apps or spreadsheets to monitor your spending habits and identify areas where you can potentially cut back.

Once you have a clear understanding of your income and expenses, integrate your estimated student loan payment into your budget. This will help you determine the impact of these payments on your overall financial situation. Consider setting up a separate savings account specifically for loan payments to make sure the funds are readily available.

Remember to build in a buffer for unexpected expenses. Life throws curveballs, and having a financial cushion can prevent you from falling behind on your loan payments during unforeseen circumstances.

Regularly review and adjust your budget as needed. Your financial circumstances may change over time, and adapting your budget accordingly is essential for long-term financial health and responsible loan management.

Choose a Repayment Plan That Fits Your Income

Graduating with student loan debt can feel overwhelming, but understanding your repayment options is crucial for managing your finances effectively. There are several repayment plans available, each designed to cater to different income levels and financial situations. Choosing the right plan can significantly impact your monthly payments and overall repayment timeline.

The standard repayment plan is a fixed payment plan spread over 10 years. While straightforward, it might result in higher monthly payments if your post-graduation income is limited. Alternatively, an income-driven repayment (IDR) plan bases your monthly payment on your income and family size. IDR plans typically offer lower monthly payments than the standard plan, but the loan repayment period might be extended to 20 or even 25 years, potentially leading to higher total interest paid.

Income-Based Repayment (IBR), Pay As You Earn (PAYE), and Revised Pay As You Earn (REPAYE) are examples of IDR plans. Each plan has specific eligibility requirements and income calculation methods. Carefully comparing these plans is essential to determine which best suits your individual circumstances. Consider factors like your expected income, family size, and long-term financial goals when making your decision. It’s recommended to thoroughly research each plan’s details and perhaps consult with a financial advisor to make an informed choice.

Remember, choosing a repayment plan is a long-term commitment. While a lower monthly payment might seem appealing initially, it’s important to consider the overall cost of the loan over the extended repayment period. Understanding the implications of each plan, such as the total interest accrued and the length of repayment, will empower you to make a financially sound decision that aligns with your post-graduation financial plan.

Avoid Common Post-Grad Loan Mistakes

Navigating the post-graduation financial landscape can be daunting, especially with outstanding student loans. Making informed decisions is crucial to avoid common pitfalls and manage your debt effectively. One of the biggest mistakes is failing to understand your loan terms. Carefully review your loan agreements to fully grasp repayment amounts, interest rates, and repayment schedules. This understanding forms the bedrock of a successful repayment strategy.

Another frequent error is neglecting to explore different repayment plans. The standard repayment plan may not be the best fit for your circumstances. Consider options like income-driven repayment plans, which adjust your monthly payments based on your income and family size. Researching and choosing the most suitable plan can significantly impact your long-term financial health. Ignoring this crucial step could lead to unnecessary financial strain.

Ignoring communication with your loan servicer is a recipe for disaster. Regularly checking your account statements, understanding updates on interest rates, and promptly addressing any discrepancies are essential for preventing late payments and damaging your credit score. Proactive communication ensures you stay informed and avoid potential complications.

Many graduates fall into the trap of prioritizing immediate gratification over long-term debt reduction. While enjoying life after college is understandable, it’s crucial to balance spending with responsible debt management. Creating a realistic budget that allocates sufficient funds towards loan repayment is vital. This prevents accumulating more debt and ensures steady progress in paying down your existing loans.

Finally, failing to plan for unexpected expenses can quickly derail your repayment strategy. Life throws curveballs, from medical emergencies to car repairs. Building an emergency fund, even a small one, provides a financial buffer and prevents you from resorting to high-interest debt to cover unexpected costs, thus delaying loan repayment.

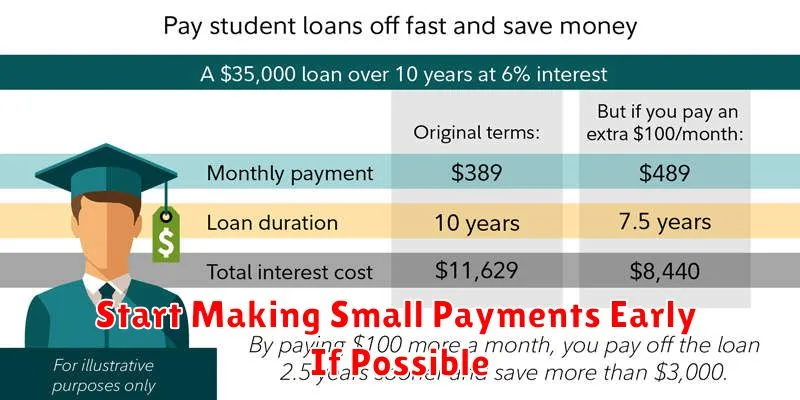

Start Making Small Payments Early If Possible

One of the most effective strategies to manage your student loan debt after graduation is to begin making payments as early as possible, even if they’re small. Many loan programs offer a grace period before repayment begins, but utilizing this time to start chipping away at the principal can significantly reduce the overall interest accrued over the life of the loan.

Even small, consistent payments can make a substantial difference in the long run. Think of it as building a positive financial habit while minimizing the burden of a large initial payment. This approach demonstrates responsible financial management and can potentially reduce the total amount you’ll need to pay back.

Furthermore, early payments, even if below the minimum required amount once the grace period ends, can demonstrate financial responsibility to lenders. This positive track record can be beneficial if you need to apply for other loans or financial assistance in the future. It also allows you to familiarize yourself with the repayment process and avoid any potential surprises or late payment penalties down the line.

Consider exploring options for making pre-payments during the grace period, especially if you have some savings or additional funds available. While you may not be able to make large payments immediately, smaller contributions add up over time and lessen your overall loan burden. This proactive approach is key to achieving long-term financial stability after graduation.

{kind=link}