Considering a personal loan to bolster your credit score? Many find themselves in a situation where improving their credit is a top priority, and a personal loan might seem like a viable option. This article will delve into the complexities of using a personal loan to build credit, exploring the potential benefits and risks involved. We’ll analyze how responsible loan management can positively impact your credit report and discuss strategies for maximizing the credit-building potential of a personal loan. Understanding these factors is crucial for making an informed decision about whether a personal loan is the right tool for your credit repair journey.

Successfully using a personal loan for credit building hinges on several key factors. On-time payments are paramount; consistent timely payments demonstrate creditworthiness to lenders and significantly improve your credit history. We will also examine the importance of choosing a loan with manageable monthly payments to avoid defaults, which can severely damage your credit score. Furthermore, we’ll assess the impact of different loan types and interest rates on your overall credit profile, helping you navigate the process of selecting the most suitable personal loan for your specific financial goals and credit situation. This guide will provide a clear understanding of whether a personal loan is a suitable strategy for your credit improvement objectives.

How Personal Loans Show Up on Credit Reports

A personal loan will appear on your credit report as a tradeline. This tradeline will include key details about the loan, impacting your credit score in several ways.

The most significant factor is your payment history. Consistent on-time payments are reported to the credit bureaus and positively contribute to your credit score. Conversely, missed or late payments are negatively reported and can significantly damage your creditworthiness.

Your credit utilization ratio, another crucial element of your credit score, is also affected. Taking out a personal loan will increase your available credit, influencing this ratio. Responsible management of this increased credit is crucial for maintaining a healthy credit score.

The loan amount and interest rate are also recorded on your credit report. These factors, while not directly impacting your score as much as payment history and credit utilization, contribute to the overall picture lenders use to assess your creditworthiness.

Finally, the length of your credit history is extended by a personal loan. A longer credit history, especially one demonstrating consistent responsible borrowing and repayment, generally leads to a higher credit score.

It’s important to remember that the impact of a personal loan on your credit report is directly tied to your ability to manage the loan responsibly. Careful planning and budgeting are essential to ensuring that a personal loan contributes positively to your credit profile.

The Impact of Timely vs Missed Payments

Your credit score is a crucial factor influencing your financial life. It significantly impacts your ability to secure loans, rent an apartment, or even get certain jobs. A personal loan can be a powerful tool in building or repairing your credit, but the success hinges entirely on your payment behavior.

Timely payments are the cornerstone of a healthy credit report. Every on-time payment acts as a positive data point, gradually boosting your credit score. Lenders see this consistency as a sign of responsibility and reliability, making you a more attractive borrower in the future. The more on-time payments you have, the higher your credit score is likely to climb.

Conversely, missed payments have a severely detrimental effect on your credit score. Even a single missed payment can negatively impact your creditworthiness for years. Credit bureaus record these instances, and lenders view them as a significant risk. Multiple missed payments can lead to a drastically lowered credit score, making it much harder to obtain future loans or credit cards at favorable interest rates.

The impact isn’t merely about the numerical score; it translates to real financial consequences. Missed payments can result in higher interest rates on future loans, making borrowing more expensive. They can also lead to collection agencies contacting you, impacting your personal relationships and potentially resulting in legal actions. In short, maintaining a consistent record of timely payments is paramount to building and maintaining a good credit score.

Therefore, understanding the profound difference between timely and missed payments is crucial when considering a personal loan for credit building. Careful planning and budgeting are essential to ensure timely payments and reap the positive effects on your credit score.

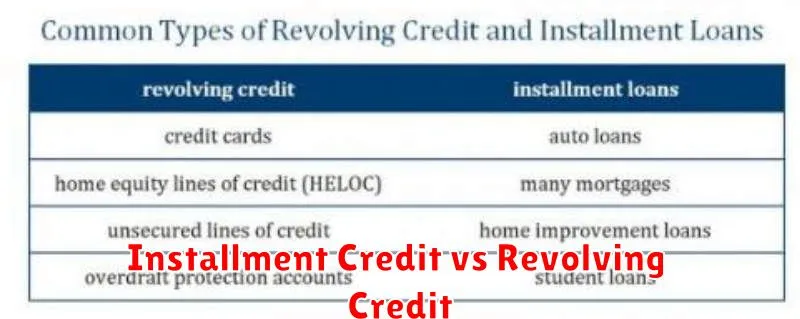

Installment Credit vs Revolving Credit

Understanding the difference between installment credit and revolving credit is crucial when considering how a personal loan can impact your credit score. Both are types of credit, but they function very differently.

Installment credit involves borrowing a fixed amount of money that you repay in regular installments over a specific period. Each payment typically covers both principal and interest. Personal loans, auto loans, and mortgages are all examples of installment credit. The key feature is the predetermined repayment schedule; you know exactly how much you owe and when you’ll be finished paying.

Revolving credit, on the other hand, allows you to borrow money up to a predetermined credit limit. You can borrow and repay as needed, repeatedly using the available credit. Credit cards are the most common example of revolving credit. Your monthly payment is typically a minimum amount, but you can pay more to reduce your balance. The available credit fluctuates as you borrow and repay.

A personal loan falls squarely into the installment credit category. This structured repayment plan can be beneficial for credit building because responsible management demonstrates your ability to handle debt effectively. Consistent on-time payments significantly contribute to a positive credit history.

While both types of credit can help you build credit, the predictability and structured repayment of installment credit like a personal loan can often make it a more straightforward path towards improving your credit score. The key is responsible borrowing and timely repayment on all credit accounts.

How Loan Term Length Affects Credit Score

The length of your loan term, or the amount of time you have to repay your loan, significantly impacts your credit score. This is because it directly affects several key factors considered in credit scoring models.

A shorter loan term generally means higher monthly payments. While this might seem daunting, it offers several benefits for your credit. First, you’ll pay less interest overall, saving you money in the long run. Second, successfully managing higher monthly payments demonstrates to lenders your ability to handle financial responsibility, which can positively affect your credit score. Finally, the shorter repayment period reduces the amount of time a loan appears on your credit report, allowing for quicker improvement in your credit utilization ratio—a critical factor in your credit score calculation.

Conversely, a longer loan term results in lower monthly payments, making the loan seem more manageable initially. However, this often leads to paying significantly more interest over the life of the loan. The extended repayment period means the loan remains on your credit report for a longer duration. While manageable payments might seem appealing, consistently making these payments over an extended period without demonstrating strong credit management skills elsewhere might not substantially boost your credit score.

Ultimately, the optimal loan term depends on your individual circumstances and financial capabilities. Carefully consider your ability to make consistent, timely payments and weigh the long-term cost of interest against the potential impact on your credit score. Responsible repayment, regardless of loan term length, is crucial for building positive credit history.

It is important to note that while loan term length is a factor, it’s only one piece of the puzzle. Your payment history, credit utilization, and the age of your credit history all play significant roles in determining your overall credit score.

Best Practices to Maximize Positive Impact

To maximize the positive impact of a personal loan on your credit score, responsible borrowing and repayment are crucial. This means carefully considering your financial situation before applying for a loan and ensuring you can comfortably afford the monthly payments.

Prioritize loan selection. Compare interest rates and terms from multiple lenders to secure the most favorable loan. A lower interest rate will reduce your overall cost and improve your credit score more quickly through timely payments.

Maintain a consistent payment history. Paying your loan installments on time, every time, is paramount. Late or missed payments will severely damage your credit score, negating any potential benefits.

Keep your credit utilization low. Avoid taking on too much debt simultaneously. High credit utilization (the percentage of available credit you’re using) can negatively impact your credit score. Consider managing existing debts to lower your overall credit utilization before applying for a personal loan.

Monitor your credit report regularly. Check your credit report frequently for accuracy and to track the progress of your credit score improvement after obtaining a personal loan. This proactive approach enables early detection of any errors that could hinder your credit building efforts.

Consider your credit mix. A diverse credit mix, including a personal loan, can positively influence your credit score, provided you manage all credit accounts responsibly. However, avoid taking on more debt than necessary.

By diligently following these best practices, you can significantly leverage a personal loan to improve your creditworthiness and build a stronger financial future.

When a Loan Might Hurt Your Credit Instead

While personal loans can be a valuable tool for credit building, it’s crucial to understand that they aren’t a guaranteed path to a higher credit score. In certain circumstances, taking out a personal loan can actually harm your credit.

One significant risk is overextending yourself financially. Applying for multiple loans simultaneously can negatively impact your credit score, as it signals to lenders that you may be struggling to manage your finances. Each credit application results in a hard inquiry, which slightly lowers your score. Simultaneously managing several loan payments can also lead to missed payments, significantly damaging your credit.

High debt-to-income ratio is another factor. If your debt payments already constitute a large portion of your income, adding another loan can push you over the edge, making it difficult to repay your existing debts and the new loan. Lenders view this as a high risk, negatively impacting your creditworthiness.

The interest rate on a personal loan plays a significant role. A high-interest loan can quickly become unmanageable, especially if unexpected expenses arise. Failing to make timely payments due to high interest burdens directly contributes to a lower credit score.

Finally, choosing a loan with unfavorable terms, such as prepayment penalties or excessive fees, can also hurt your credit in the long run. These unexpected costs can strain your finances and lead to missed payments, negatively impacting your credit report.

{kind=link}