Are you struggling with high-interest credit card debt? Many find themselves overwhelmed by mounting balances and minimum payments that barely make a dent. A personal loan might seem like a tempting solution, offering the potential for lower interest rates and a manageable monthly payment plan. But is it the right financial move for you? This article delves into the pros and cons of using a personal loan to consolidate and pay off your credit card debt, helping you make an informed decision about your financial future.

Before you consider taking out a personal loan, it’s crucial to carefully weigh the benefits and risks. We’ll explore factors like your credit score, interest rates, and the potential impact on your overall financial health. Understanding the intricacies of debt consolidation and the implications of adding another loan to your financial profile is vital. This comprehensive guide will equip you with the knowledge necessary to determine whether a personal loan is the best strategy for tackling your credit card debt and achieving financial freedom.

Why People Consider Debt Consolidation

Many people consider debt consolidation as a way to simplify their finances and potentially save money. The primary driver is the management of multiple debts with varying interest rates and due dates. Juggling several accounts can be overwhelming, leading to missed payments and further financial strain.

A significant advantage is the potential for lower interest rates. Consolidating debt into a single loan, such as a personal loan, often offers a lower interest rate than the individual credit card rates. This can lead to substantial savings over the repayment period, accelerating debt reduction.

Simplified payments are another key attraction. Instead of multiple monthly payments to different creditors, consolidating allows for a single, manageable monthly payment. This simplified approach improves budgeting and reduces the risk of missed payments, which can negatively impact credit scores.

Debt consolidation can also offer improved financial clarity. By combining all debts into one, individuals gain a clearer understanding of their overall debt burden and repayment schedule. This transparency empowers better financial planning and decision-making.

Finally, some find that debt consolidation offers a sense of psychological relief. The simplification of their financial situation can alleviate stress and anxiety associated with managing multiple debts, contributing to improved overall well-being.

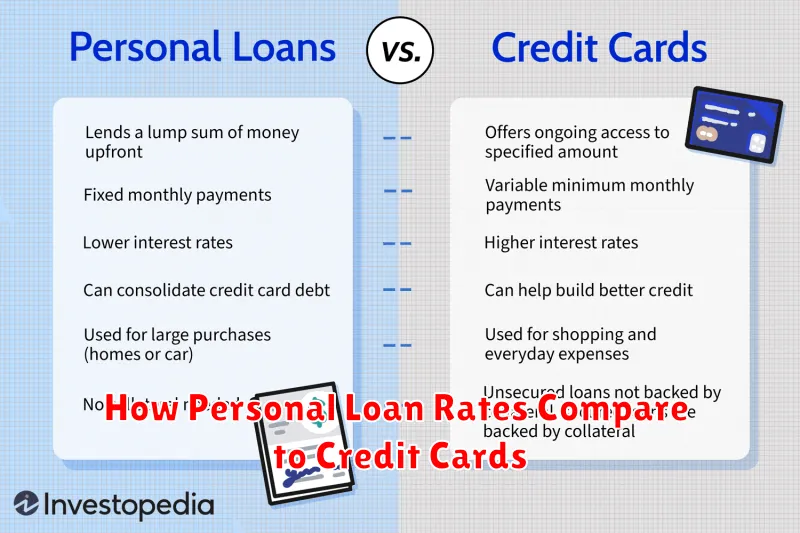

How Personal Loan Rates Compare to Credit Cards

Understanding the difference between personal loan interest rates and credit card interest rates is crucial when deciding whether to consolidate your credit card debt. Credit cards typically carry significantly higher interest rates than personal loans.

While credit card APRs (Annual Percentage Rates) can fluctuate and often exceed 20%, personal loan interest rates are generally fixed and considerably lower. This fixed rate provides predictability, allowing you to accurately budget your monthly payments and know exactly how much interest you’ll pay over the loan’s lifetime.

The specific interest rate you qualify for with a personal loan depends on several factors, including your credit score, income, and the loan amount. However, even borrowers with less-than-perfect credit often find personal loan rates more favorable than their existing credit card rates.

Furthermore, personal loans offer a defined repayment period, meaning you’ll pay off your debt within a set timeframe. This structured approach contrasts with credit cards, where minimum payments can prolong debt repayment significantly and accumulate substantial interest charges over time.

Therefore, a careful comparison of your current credit card APR and the offered personal loan interest rate is essential to determine if debt consolidation through a personal loan is financially advantageous. A lower interest rate, combined with a fixed repayment schedule, can lead to considerable savings on interest payments and faster debt elimination.

Pros: Fixed Payments, Lower Interest

One of the most significant advantages of using a personal loan to consolidate high-interest credit card debt is the potential for lower interest rates. Credit cards often carry significantly higher interest rates than personal loans. This means you could save a substantial amount of money on interest payments over the life of the loan.

Furthermore, personal loans typically offer fixed monthly payments. This predictability is a major benefit for budgeting. Unlike credit cards, where minimum payments can fluctuate and interest charges can vary, a fixed payment amount allows for better financial planning and reduces the risk of unexpected increases in your monthly expenses.

The simplicity of managing a single monthly payment, as opposed to multiple credit card payments, is another key advantage. This streamlined approach can make debt repayment less stressful and easier to track. This simplified repayment process can contribute to improved financial organization and reduced chances of missed payments.

Finally, successfully paying off a personal loan can have a positive impact on your credit score. On-time payments demonstrate responsible financial behavior to credit bureaus, which can help you qualify for better interest rates and credit opportunities in the future.

Cons: New Loan, Possible Fees

Taking out a personal loan to consolidate your credit card debt introduces a new debt obligation. While this simplifies payments into one monthly installment, it also means adding another loan to your financial profile. Managing this new loan responsibly requires careful budgeting and adherence to the repayment schedule to avoid further financial difficulties.

Fees associated with personal loans can significantly impact the overall cost. Origination fees, prepayment penalties, and late payment fees can quickly add up, potentially negating some of the benefits of consolidation. Carefully review the loan agreement to understand all associated fees before committing to the loan.

Furthermore, obtaining a personal loan might temporarily lower your credit score. The inquiry into your credit history from the lender, and the addition of a new loan account, can both affect your credit rating. While responsible repayment can quickly improve your score later, the initial dip should be considered.

Lastly, it’s crucial to consider the interest rate of the personal loan. While a lower interest rate compared to your credit card rates can be beneficial, it’s essential to compare interest rates from multiple lenders to ensure you’re securing the best possible deal. A higher interest rate on the personal loan could ultimately make debt payoff more costly and time-consuming.

How to Avoid Rebuilding Credit Card Debt

Successfully paying off credit card debt is a significant achievement, but the work doesn’t end there. Preventing the accumulation of new debt is crucial to maintaining a healthy financial standing. Careful budgeting and disciplined spending habits are paramount.

Creating a Realistic Budget is the cornerstone of avoiding future debt. Track your income and expenses meticulously to identify areas where you can cut back. This includes identifying non-essential spending and prioritizing essential needs like housing, food, and transportation. Utilize budgeting apps or spreadsheets to simplify this process.

Building an Emergency Fund provides a safety net to handle unexpected expenses without resorting to credit cards. Aim for 3-6 months’ worth of living expenses in a readily accessible savings account. This prevents the need to borrow money for emergencies, a common cause of credit card debt relapse.

Utilizing Alternative Payment Methods can help curb impulsive purchases. Consider using cash or debit cards instead of credit cards for everyday transactions. This added friction can encourage more thoughtful spending habits. Avoid using “buy now, pay later” services as these often mirror credit card debt cycles.

Regularly Monitoring Credit Reports and Statements allows for early detection of any potential issues. Review your credit card statements thoroughly for accuracy and any unauthorized charges. Checking your credit report annually can help you identify potential problems and address them before they escalate.

Seeking Professional Financial Guidance can provide valuable support and personalized strategies for long-term financial health. A financial advisor can help develop a comprehensive financial plan to manage expenses and prioritize debt repayment. They can also offer advice on investment strategies and retirement planning.

When Consolidation Makes the Most Sense

Consolidating your credit card debt with a personal loan can be a strategic move, but it’s not always the best solution. The most compelling reasons to consolidate involve achieving significant financial benefits.

One key advantage is a lower interest rate. If your personal loan offers a significantly lower interest rate than your credit cards, you’ll save money on interest charges over time. This is especially true if you have multiple high-interest credit cards.

Another benefit is simplification. Managing multiple credit card payments can be complicated. A single monthly payment simplifies your finances, making budgeting and tracking your progress easier. This streamlined approach can reduce the risk of missed payments and associated late fees.

Consolidation can also be beneficial if you are struggling with debt management. A fixed-term loan with a clear repayment plan can provide a sense of control and structure, helping you stay on track and avoid further debt accumulation.

However, it’s crucial to carefully consider the terms of the personal loan. Make sure the interest rate is truly lower than your credit card rates, factoring in any fees. Also, ensure the loan term allows you to comfortably repay the debt without stretching your budget too thin.

Finally, while consolidating can improve your credit score by simplifying your debt profile, it only works if you maintain responsible repayment behavior. Defaulting on your personal loan will severely damage your credit, creating an even bigger financial problem.

{kind=link}