Planning for a personal loan can be a daunting task, especially when you’re concerned about maintaining a healthy budget. Many individuals shy away from borrowing due to fears of debt and potential financial instability. However, with careful planning and a realistic understanding of your financial situation, securing a personal loan without derailing your budget is entirely achievable. This guide provides practical steps to navigate the loan application process effectively and responsibly, helping you make informed decisions that support your financial goals.

This article will equip you with the tools and knowledge to successfully manage your personal finances while pursuing a personal loan. We’ll explore crucial factors such as determining your affordability, comparing loan interest rates and terms, and building a comprehensive budget that accommodates your loan repayment schedule without sacrificing essential expenses. Understanding your credit score and its impact on loan approval is also vital, and we’ll delve into strategies to improve your creditworthiness if necessary. Ultimately, our goal is to empower you to make sound financial choices that lead to a positive loan experience.

Know the Exact Purpose of the Loan

Before you even begin considering a personal loan, it’s crucial to clearly define its purpose. Avoid vague intentions; instead, specify exactly what the loan will finance. This clarity is essential for several reasons.

Firstly, a well-defined purpose helps you determine the necessary loan amount. Knowing precisely what you need to fund prevents you from borrowing more than necessary, thus minimizing interest payments and overall debt burden. Overestimating your needs can lead to significant financial strain later.

Secondly, a clear purpose allows you to compare loan offers more effectively. Different lenders offer varying interest rates and repayment terms. By understanding your specific needs, you can focus on offers that best align with your financial goals and budget. This focused approach improves your chances of securing a loan with favorable terms.

Thirdly, a clearly defined purpose simplifies the loan application process. Lenders often require applicants to explain how they intend to use the funds. A well-articulated purpose enhances your credibility and strengthens your application, potentially leading to a quicker and smoother approval process.

Finally, having a specific purpose helps you stay accountable. Knowing exactly why you borrowed the money encourages responsible spending and repayment. It minimizes the risk of misusing the funds and accumulating further debt.

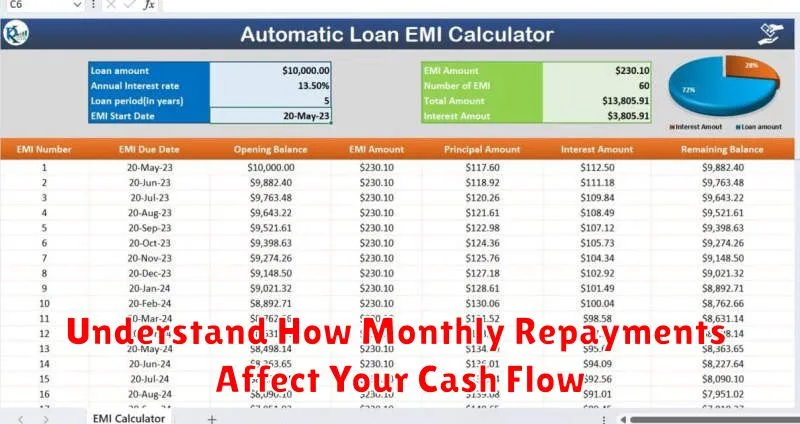

Understand How Monthly Repayments Affect Your Cash Flow

Before taking out a personal loan, it’s crucial to understand how the monthly repayments will impact your cash flow. This involves carefully assessing your current income and expenses to determine your affordability.

Start by creating a detailed budget that outlines all your monthly income and expenses. This should include fixed costs such as rent or mortgage payments, utilities, and transportation, as well as variable expenses like groceries, entertainment, and dining out. Accurately tracking your spending for a month or two beforehand will provide a realistic picture of your financial situation.

Once you have a clear understanding of your current cash flow, you can then incorporate the projected loan repayment amount into your budget. Subtract the monthly payment from your net income (income after taxes and deductions) to determine your remaining disposable income. This will show you how much money you will have left each month for other expenses and savings.

Consider using a budgeting tool or spreadsheet to help visualize the impact of the loan payment on your monthly cash flow. This will allow you to make informed decisions about whether you can comfortably afford the loan without compromising your financial stability or other important financial goals.

It’s also wise to factor in a buffer or contingency fund. Unexpected expenses can easily arise, and having extra funds can prevent you from falling behind on your loan payments or jeopardizing your budget. A healthy emergency fund can help alleviate financial stress.

Remember, a manageable loan payment should leave you with sufficient funds to cover your essential living expenses and still have some money left over for savings and other priorities. If incorporating the loan payment significantly strains your budget, consider exploring alternative options, such as reducing the loan amount, extending the loan term (although this may increase the total interest paid), or delaying the loan until your financial situation improves.

Factor in Fees and Insurance

Before you sign on the dotted line, it’s crucial to understand the full cost of your personal loan. Many lenders charge various fees, such as origination fees, application fees, or prepayment penalties. These fees can significantly impact the total amount you end up paying. Carefully review the loan agreement and inquire about any potential hidden fees.

Consider the possibility of loan insurance. While some lenders might offer it as a requirement, others may present it as an optional add-on. Loan insurance protects the lender if you’re unable to repay the loan, but it comes with an additional cost, increasing your monthly payments. Weigh the benefits and the extra expense before deciding whether to opt for this protection.

To accurately assess the true cost of your loan, add all anticipated fees and insurance premiums to the principal loan amount. This will give you a realistic total cost, allowing for a more accurate budget projection. Don’t let seemingly small fees mislead you; they can accumulate, and it’s vital to account for them from the beginning. This thorough approach will ensure your personal loan aligns with your financial capabilities and avoids unexpected financial strain.

Use a Loan Calculator to Forecast Expenses

Before you apply for a personal loan, it’s crucial to utilize a loan calculator to accurately forecast your monthly expenses. This tool allows you to input key variables, such as the loan amount, interest rate, and loan term, to generate a detailed repayment schedule.

Understanding your projected monthly payment is vital for budgeting. The calculator will clearly show the principal and interest components of each payment, providing a comprehensive overview of your financial obligations. This allows you to realistically assess whether the loan fits within your current financial capacity without causing undue strain on your budget.

Furthermore, a loan calculator can help you explore different loan scenarios. By adjusting the loan term or interest rate, you can see how these changes impact your monthly payment. This experimentation enables you to make informed decisions, potentially finding a loan option that better aligns with your financial goals and minimizes the risk of overextending yourself.

Many free online loan calculators are readily available, providing a convenient and effective way to plan for your loan expenses. Taking the time to use this tool is an essential step in responsible borrowing and prevents potential financial difficulties down the line.

When to Delay Borrowing Until You’re Ready

Taking out a personal loan can be a significant financial decision, and it’s crucial to ensure you’re fully prepared before committing. Delaying borrowing until you’re ready can prevent a cascade of negative financial consequences.

One key indicator is your debt-to-income ratio (DTI). A high DTI, meaning a large portion of your income is already dedicated to paying off debts, makes it riskier to take on additional borrowing. Carefully evaluate your existing debts and your ability to manage repayments before considering a personal loan.

Your credit score is another critical factor. A low credit score often leads to higher interest rates and less favorable loan terms. Improving your credit score before applying for a loan can save you considerable money in the long run. Take steps to address any negative items on your report before seeking financing.

Consider your emergency fund. Unexpected expenses can easily derail your loan repayment plan. Having a robust emergency fund provides a financial buffer and reduces the risk of falling behind on payments. It’s wise to have 3-6 months of living expenses saved before taking on new debt.

Finally, ensure you have a clear understanding of the loan terms, including interest rates, fees, and repayment schedule. Thoroughly research different lenders and compare options before making a decision. Don’t rush the process; take the time to understand the implications of the loan before signing.

How to Include Repayments in Your Budget Plan

Successfully incorporating loan repayments into your budget requires careful planning and a realistic assessment of your financial situation. Begin by determining your monthly repayment amount, including principal and interest. This information is typically provided in your loan agreement.

Next, analyze your current income and expenses. Create a detailed budget that outlines all your regular monthly income sources and expenses. Categorize your expenses to identify areas where you might be able to reduce spending to accommodate the loan payments.

Once you have a clear picture of your finances, integrate the loan repayment amount into your budget. Treat it as a non-negotiable expense, similar to rent or utilities. Dedicate a specific line item for loan repayments to ensure you consistently allocate the necessary funds.

Consider using budgeting tools or apps to assist you in tracking your income and expenses. These tools can help you visualize your financial situation and ensure you remain on track with your repayment schedule. Regularly review and adjust your budget as needed, especially during periods of unexpected financial changes.

It is crucial to prioritize your loan repayments. Missed payments can result in late fees and damage your credit score. If you anticipate difficulties making payments, immediately contact your lender to discuss potential solutions, such as a repayment plan modification.

Remember that responsible budgeting is key to managing a personal loan effectively. By carefully planning and tracking your finances, you can incorporate loan repayments into your budget without compromising your other financial obligations.

{kind=link}