Understanding the intricacies of property taxes can be daunting, especially when they’re bundled into your monthly mortgage payments. This often overlooked aspect of homeownership significantly impacts your overall housing costs. This article aims to demystify the complexities of property tax assessments, tax rates, and how these factors influence your monthly mortgage payment. We’ll explore how your property tax bill is calculated, common misconceptions surrounding property taxes, and strategies for managing and potentially lowering your annual property tax burden. Learn how to navigate the financial landscape of homeownership with greater confidence by gaining a clearer picture of this essential component of your mortgage.

Knowing exactly what comprises your monthly mortgage payment is crucial for effective financial planning. This guide provides a comprehensive breakdown of property taxes within your mortgage, explaining the relationship between property value, tax rates, and your escrow account. We will discuss the implications of property tax increases on your budget and how to budget for unexpected fluctuations. Furthermore, we’ll delve into the various ways to appeal a property tax assessment if you believe it is inaccurate, potentially leading to significant cost savings over the life of your loan. Understanding these factors empowers you to make informed decisions about your homeownership journey.

Why Lenders Collect Property Taxes

Lenders require borrowers to pay their property taxes as part of their monthly mortgage payments through a process called escrow. This isn’t simply a matter of convenience for the lender; it’s a crucial risk mitigation strategy.

The primary reason lenders collect property taxes is to protect their investment. If property taxes go unpaid, the local government can place a lien on the property. This lien takes priority over the mortgage, meaning the government would be paid first if the property were foreclosed upon. This could leave the lender with a significant financial loss if the sale proceeds aren’t sufficient to cover both the taxes and the mortgage.

By collecting property taxes in escrow, lenders ensure the timely payment of these essential fees. This safeguards their collateral (the property) and minimizes the risk of default due to unpaid taxes. It streamlines the process, eliminating the need for the borrower to track multiple due dates and payment methods.

Furthermore, escrow accounts offer convenience for the borrower. Instead of managing separate payments for the mortgage and property taxes, borrowers make a single monthly payment that covers both. This simplifies budgeting and reduces the risk of missed payments, which could lead to late fees or damage to credit scores.

In essence, the lender’s collection of property taxes is a mutually beneficial arrangement that protects the lender’s investment while providing borrowers with a streamlined and convenient payment system.

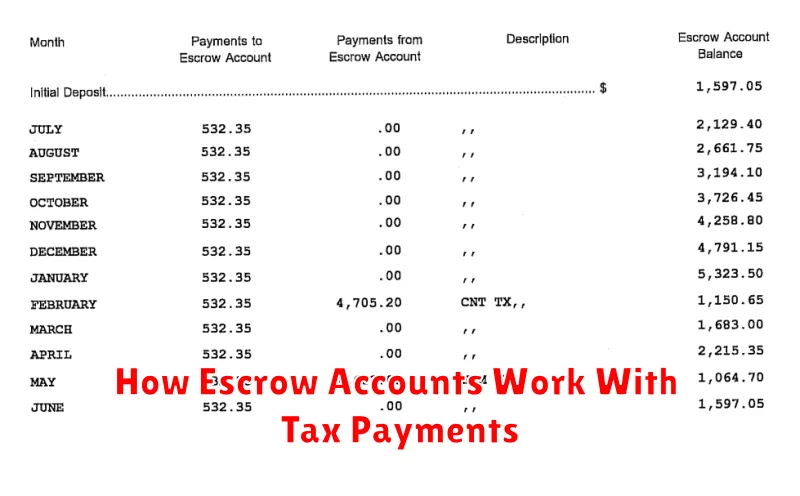

How Escrow Accounts Work With Tax Payments

When you take out a mortgage, your lender may require you to set up an escrow account. This is a separate account held by your lender where you make monthly payments that cover not only your principal and interest but also your property taxes and homeowners insurance.

The escrow process simplifies the payment of these bills. Instead of remembering to pay your property taxes and insurance premiums twice a year or annually, your lender collects these payments along with your mortgage payment. They then pay your property taxes and insurance premiums on your behalf at the appropriate times.

Your lender estimates the annual property tax and insurance costs when you close on your loan and divides that amount by 12 to determine your monthly escrow payment. They may adjust this amount periodically based on your tax and insurance bills.

It’s crucial to understand that the money in your escrow account belongs to you, although it’s held by the lender. They are legally obligated to use these funds only for their intended purpose: paying your property taxes and insurance premiums. You usually receive an annual statement showing the amount paid out of your escrow account for taxes and insurance.

Failure to maintain sufficient funds in your escrow account can lead to the lender requiring additional payments to bring the account up to date. Severe deficiencies may result in the lender taking action to ensure the taxes and insurance are paid, potentially affecting your credit score.

Regularly reviewing your escrow account statements is recommended to ensure the lender is accurately managing your funds and paying your bills on time. Any discrepancies should be reported to the lender promptly.

How Property Taxes Are Calculated

Understanding how property taxes are calculated is crucial for budgeting and managing your mortgage payments. The process involves several key components, and the exact formula can vary slightly depending on your location.

The foundation of the calculation is the assessed value of your property. This is an estimate of your property’s market value, determined by your local government’s assessor. This value is not always identical to your home’s purchase price or recent appraisal; it’s a standardized assessment for tax purposes.

Next, the assessed value is multiplied by the tax rate. The tax rate is expressed as a millage rate (mills per dollar of assessed value) or a percentage. A mill is one-tenth of a cent ($0.001). For instance, a tax rate of 20 mills means that for every $1,000 of assessed value, you’ll pay $20 in property taxes.

Exemptions can significantly reduce your taxable value. These exemptions may be based on factors such as age, veteran status, or disability. The specific exemptions and their amounts vary greatly depending on your state and local government regulations.

Finally, the calculation might include additional fees and levies. These extra charges are often added to the base property tax calculation. These can include things such as school district levies, special assessments for local improvements, or other municipal charges.

Therefore, your total annual property tax bill represents the sum of the base tax, taking into account any applicable exemptions, plus any additional fees or levies. It’s essential to contact your local tax assessor’s office for specific details regarding your property’s assessed value, tax rates, and any potential exemptions in your area.

When Tax Assessments Change

Your property tax assessment is a crucial factor in determining the amount you pay annually. Assessments are the official valuation of your property by your local government, and these valuations can change. Changes are typically triggered by several factors including market fluctuations, improvements made to your property (additions, renovations), or reassessments of properties within the area.

Market fluctuations are perhaps the most common cause of assessment changes. If property values rise in your area, your assessment is likely to increase, leading to higher property taxes. Conversely, if property values decrease, your assessment might decrease, resulting in lower taxes. These changes are typically part of a cyclical process, reflecting the ebb and flow of the local real estate market.

Improvements you make to your home, such as additions, renovations, or significant landscaping projects, will generally result in a higher property tax assessment. This is because these improvements increase the overall value of your property. It’s important to accurately report these changes to your local assessor’s office to ensure your assessment accurately reflects the improved value.

Periodic reassessments are conducted by local governments to update property valuations across a jurisdiction. These reassessments ensure that assessments remain relatively fair and reflect current market conditions. The frequency of reassessments varies by location, but they often happen every few years or even annually.

When your property tax assessment changes, you will usually receive a notification from your local assessor’s office. This notification will outline the new assessment and how it will affect your property tax bill. It’s vital to review this notification carefully and understand the basis for the change. If you believe there is an error in the assessment, you have the right to appeal the decision through the established appeals process.

What Happens If You Pay Off Your Mortgage?

Paying off your mortgage is a significant financial achievement, triggering several important changes. The most immediate consequence is the elimination of your monthly mortgage payment. This frees up a substantial amount of your monthly budget, allowing you to allocate funds towards other financial goals, such as saving for retirement, investing, or paying down other debts.

Beyond the immediate financial relief, paying off your mortgage also significantly reduces your overall financial risk. You no longer face the risk of foreclosure due to missed payments or financial hardship. This provides a sense of security and financial stability, particularly during times of economic uncertainty.

However, the impact on your property taxes remains unchanged. Even without a mortgage, you are still responsible for paying your annual property taxes. These taxes are a separate obligation determined by your local government and are unrelated to your mortgage. You will continue to receive tax bills from your local taxing authority, and failure to pay these taxes can lead to penalties and liens on your property, just as with a mortgaged property.

It is crucial to understand that while paying off your mortgage eliminates your monthly mortgage payments, it does not eliminate your property tax liability. Managing your property taxes effectively remains an essential part of homeownership, regardless of your mortgage status.

Tips for Reviewing Your Annual Escrow Statement

Your annual escrow statement is a crucial document that details the funds your lender has collected and disbursed on your behalf for property taxes and homeowner’s insurance. Carefully reviewing this statement is essential to ensure accuracy and identify any potential issues.

Check the accuracy of the tax amounts: Verify that the property tax amounts listed on the statement match your tax bill from your local taxing authority. Discrepancies could indicate errors in either document, necessitating immediate action.

Review insurance premiums: Confirm that the insurance premiums shown are correct and reflect your current coverage. Any changes to your policy, such as increased coverage or deductible amounts, should be reflected in the escrow payments.

Examine the payment history: The statement should show a clear record of all payments made throughout the year. Review this section to ensure that all payments were processed correctly and timely. Note any late payments or discrepancies.

Look for any unusual activity: Be vigilant for anything out of the ordinary, such as unexpectedly high or low payments, or payments made to unfamiliar entities. Such anomalies might indicate a problem that needs addressing.

Understand your escrow account balance: The statement should display the current balance in your escrow account. This helps you understand your payment schedule and if any adjustments are required.

Compare year-over-year changes: By comparing your current statement to previous years’ statements, you can track changes in property taxes and insurance premiums and easily spot any significant variations needing explanation.

Contact your lender promptly: If you notice any discrepancies or errors on your statement, don’t hesitate to contact your lender immediately to address the concerns. Early resolution is crucial to prevent future complications.

{kind=link}