Rebuilding your credit score can feel like an uphill battle, but a secured credit card can be a powerful tool in your arsenal. This helpful guide will walk you through the process of using a secured credit card to effectively rebuild your credit history. We’ll cover everything from choosing the right card and understanding your credit limit to mastering responsible credit card use and monitoring your credit report for progress. Learn how to leverage this financial instrument to improve your creditworthiness and unlock access to better financial opportunities in the future.

Many people with damaged credit or limited credit history find themselves struggling to obtain traditional credit products. A secured credit card, however, requires a security deposit, essentially guaranteeing the issuer against potential losses. This makes it a readily accessible option for those looking to establish or improve their credit. By demonstrating responsible credit card usage—such as paying your bills on time and keeping your credit utilization ratio low—you can significantly improve your credit rating over time. This article will equip you with the knowledge and strategies to effectively use a secured credit card to achieve your credit-building goals.

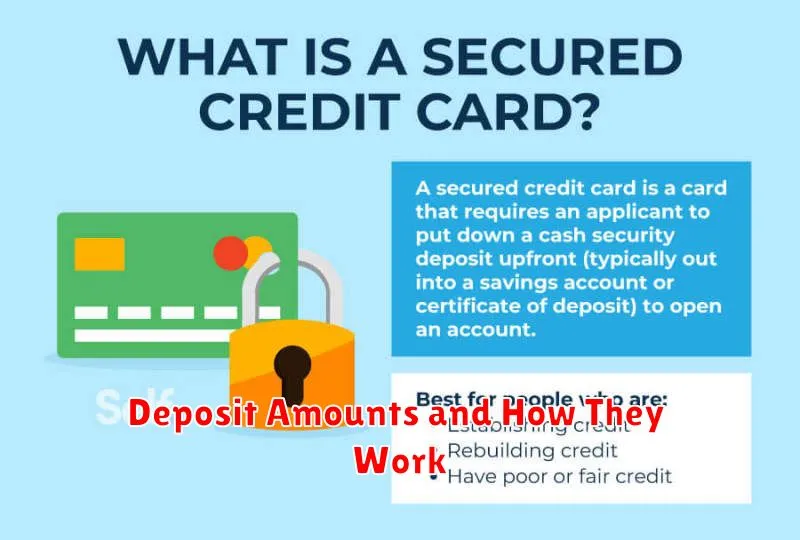

What Is a Secured Credit Card?

A secured credit card is a type of credit card that requires a security deposit. This deposit, which typically ranges from $200 to $500, serves as your credit limit. Unlike unsecured credit cards, which are offered based on your creditworthiness, secured cards are available to almost everyone, regardless of their credit history.

The key difference between a secured and an unsecured credit card lies in the security deposit. This deposit acts as a guarantee for the credit card issuer, mitigating their risk. If you fail to make payments, the issuer can use the deposit to cover your outstanding balance.

Secured credit cards offer a valuable tool for individuals looking to rebuild their credit. By using the card responsibly and making on-time payments, you can establish a positive credit history, which can subsequently lead to approval for unsecured credit cards with better terms and benefits. Responsible usage includes paying your balance in full and on time each month, keeping your credit utilization low, and avoiding exceeding your credit limit.

It’s important to note that while a secured credit card offers a path to improved credit, it typically comes with higher fees compared to unsecured credit cards. These fees may include an annual fee and/or a higher interest rate. Carefully review the terms and conditions of any secured credit card before applying to ensure it aligns with your financial goals.

Choosing the right secured credit card involves comparing fees, interest rates, and credit reporting practices. Some secured cards report to all three major credit bureaus (Equifax, Experian, and TransUnion), which is crucial for building your credit score effectively. Others may only report to one or two, potentially impacting the speed of your credit rebuilding journey.

How It Helps Build Credit History

A secured credit card is a powerful tool for building credit history, especially for individuals with limited or damaged credit. Unlike many other financial products, secured cards are designed to be accessible even to those with low credit scores or no credit history at all.

The key is responsible use. By making timely payments on your secured credit card balance each month, you demonstrate to credit bureaus (like Experian, Equifax, and TransUnion) your ability to manage credit responsibly. This positive payment history is a crucial factor in your credit score calculation.

Moreover, the credit utilization ratio – the percentage of your available credit that you use – is another important element of your credit score. Using a secured card responsibly, meaning keeping your utilization low (ideally below 30%), further strengthens your credit profile. The consistent and responsible use of a secured card showcases your creditworthiness to lenders.

Finally, the length of your credit history is also a factor in determining your credit score. By maintaining a secured credit card account in good standing over time, you gradually build a longer credit history, positively impacting your overall creditworthiness. This length of history, coupled with positive payment behavior and low utilization, can significantly improve your credit score over time.

Deposit Amounts and How They Work

Secured credit cards require an initial security deposit. This deposit acts as collateral, guaranteeing the credit card issuer that you will pay your balance. The amount of the deposit directly influences your credit limit; it’s typically equal to or a multiple of your deposit.

For example, a $200 deposit might result in a $200 credit limit, or sometimes a slightly higher limit depending on the issuer’s policies. Some issuers may offer credit limits that are higher than the deposit amount, but this is less common. It’s crucial to understand the specific terms and conditions of your chosen card to avoid any surprises.

The minimum deposit amount varies greatly among card issuers. Some may require as little as $200, while others may have higher minimums, reaching $500 or more. Always check the card’s details before applying to ensure you can comfortably afford the initial deposit.

Your deposit remains secured with the issuer for the duration of your account. It is not considered an interest-bearing account; you won’t earn interest on your deposit. Upon closing your account in good standing (meaning you’ve paid off your balance), the issuer will typically return your deposit in full.

While the deposit acts as a safety net for the issuer, responsible spending is still crucial. Failing to make timely payments could lead to negative impacts on your credit score. Even with a secured card and deposit, consistent late payments can damage your credit history.

Tips for Responsible Usage

Using a secured credit card responsibly is crucial for rebuilding your credit. It’s not just about making payments; it’s about demonstrating consistent and reliable financial behavior to credit bureaus.

Pay on time, every time: This is the single most important factor affecting your credit score. Set up automatic payments or reminders to ensure you never miss a due date. Even one late payment can significantly impact your progress.

Keep your credit utilization low: Credit utilization refers to the percentage of your available credit that you’re using. Aim to keep this below 30%, ideally much lower. A high utilization ratio signals to lenders that you may be overextended financially.

Monitor your account regularly: Check your statement each month for accuracy and to track your spending. This helps you identify any potential errors or unauthorized charges promptly.

Avoid applying for additional credit: While rebuilding your credit, avoid applying for new credit cards or loans. Each application results in a hard inquiry on your credit report, which can temporarily lower your score. Focus on responsible usage of your secured card.

Understand your credit limit: Don’t exceed your credit limit. Doing so can negatively affect your credit score and incur additional fees. Stay within your approved spending limit at all times.

Consider using your card for small, regular purchases: This helps demonstrate consistent, responsible credit usage. However, avoid impulse buys or spending beyond your means.

Be patient: Rebuilding your credit takes time. Consistent responsible usage will eventually show positive results. Don’t get discouraged by slow initial progress.

When to Ask for an Upgrade or Refund

Knowing when to ask for an upgrade or refund on your secured credit card is crucial for maximizing its benefits and managing your finances effectively. Timing is key; you should not expect an upgrade or refund prematurely.

Consider requesting an upgrade after you’ve consistently demonstrated responsible credit behavior for 6-12 months. This typically involves making on-time payments, keeping your credit utilization low (ideally below 30%), and avoiding any missed payments. When you apply for an upgrade, be prepared to provide evidence of your improved creditworthiness.

A refund on the security deposit is usually only possible once you have closed your account in good standing and met the terms and conditions of your card agreement. This often requires maintaining a zero balance for a specified period. Before closing the account, verify the exact procedure and timeframe for receiving your deposit back with your credit card issuer. Contacting customer service beforehand is highly recommended to avoid any surprises.

Remember that an upgrade doesn’t automatically guarantee a refund of your security deposit. Likewise, a negative impact on your credit report might make an upgrade or a timely refund less likely. Therefore, consistent responsible credit card use is paramount.

Finally, always review the terms and conditions of your specific secured credit card agreement. The specific requirements and processes for upgrades and refunds can vary depending on your card issuer and the type of card you hold. Understanding these terms will help you know exactly when and how to make your request.

Tracking Credit Score Progress

Building your credit back up with a secured credit card requires patience and consistency. Regularly monitoring your credit score is crucial to understanding your progress and making necessary adjustments.

Several methods allow you to track your credit score effectively. You can utilize the free credit score offered by your credit card issuer, or explore services such as Credit Karma or Experian, which often provide free credit reports and scores, although the specifics can vary.

Frequency of monitoring is key. Aim to check your credit score at least once a month to observe the trend of your score improvement. This allows you to identify any potential issues early and take corrective action.

Beyond the numerical score, pay close attention to the factors that comprise your credit score. These typically include payment history, amounts owed, length of credit history, credit mix, and new credit. Understanding how each of these factors contributes to your overall score empowers you to make informed financial decisions.

Remember, building credit is a journey, not a race. Consistent responsible credit card usage, including making timely payments and keeping your credit utilization low, is the most effective strategy to see sustained improvement in your credit score over time. Tracking your progress provides vital feedback and helps maintain motivation throughout the process.

{kind=link}