Changing careers can be an exciting but daunting endeavor, especially when student loan debt is a significant factor. Many professionals find themselves wrestling with the financial implications of a career shift, questioning how to manage their student loan repayments while navigating a new professional path. This comprehensive guide provides practical strategies to effectively handle your student loans during a career transition, allowing you to pursue your dream career without being overwhelmed by financial burdens. We will explore various options, from income-driven repayment plans to potential deferment or forbearance, helping you make informed decisions that align with your financial goals and career aspirations.

This article will delve into the intricacies of managing student loan debt while pursuing a career change. We’ll address key concerns such as the impact of reduced income on loan repayments, strategies for budgeting and prioritizing payments, and the exploration of potential loan forgiveness programs. Understanding your rights and options is crucial, and we’ll guide you through the process of navigating student loan servicers and understanding your loan terms. Whether you are considering a complete career overhaul or a gradual transition, this guide offers valuable insights and actionable advice to help you successfully manage your student loan debt during this significant life change.

Reassessing Your Budget During Transition

A career change often necessitates a budget reassessment. Your income may fluctuate during the transition period, potentially decreasing as you leave your old job or start a new one with a lower salary. Simultaneously, your expenses might increase due to the costs associated with acquiring new skills, networking, or relocating for a new position.

Begin by creating a detailed spending plan. Track all your income sources, including any unemployment benefits, savings withdrawals, or part-time income. Categorize your expenses meticulously, identifying essential and non-essential costs. This will provide a clear picture of your current financial standing and allow you to pinpoint areas where you can potentially cut back.

Consider implementing temporary cost-cutting measures. This might involve reducing dining out, canceling subscriptions, or postponing non-essential purchases. Explore options for reducing housing costs, such as downsizing or finding a roommate. Such measures, while sometimes difficult, can create much-needed financial breathing room during the transition.

Prioritize your student loan payments. Depending on your financial situation and loan terms, you may explore options such as forbearance or deferment. Contact your loan servicer to discuss your options and understand the potential implications of delaying payments. It’s crucial to remain proactive and communicative with your lender to avoid accumulating penalties and further debt.

Seek professional advice if needed. A financial advisor can offer personalized guidance tailored to your circumstances. They can help you develop a sustainable budget, explore debt management strategies, and plan for long-term financial stability, ensuring that your student loans are managed effectively alongside the financial challenges of a career change.

Temporary Repayment Relief Options

Changing careers can often lead to a period of financial instability. If your new job pays less than your previous one, or if you’re temporarily unemployed while transitioning, managing your student loan repayments can become a significant challenge. Fortunately, several temporary repayment relief options exist to help you navigate this difficult time.

One option to consider is a deferment. A deferment postpones your loan payments for a specified period, typically requiring you to demonstrate financial hardship or enrollment in school. Interest may or may not accrue during a deferment, depending on your loan type. It’s crucial to understand the terms and conditions of your specific loan to determine whether accrued interest will be capitalized (added to your principal balance).

Another possibility is a forbearance. Similar to a deferment, a forbearance allows you to temporarily suspend or reduce your payments. However, forbearance is generally granted for reasons other than financial hardship, such as a medical emergency or natural disaster. Again, interest may or may not accrue during a forbearance, depending on your loan type and the specific terms of your forbearance agreement. It’s essential to explore the implications carefully before applying.

Before pursuing either a deferment or forbearance, thoroughly research your eligibility requirements. Contact your loan servicer directly to discuss your circumstances and understand the available options and the potential long-term implications of choosing either route. This includes understanding how deferments and forbearances can affect your credit score and the overall repayment timeline of your student loan.

Remember, utilizing temporary repayment relief should be viewed as a short-term solution. Creating a budget and developing a long-term repayment plan as soon as possible is crucial to regain financial stability and avoid accumulating excessive interest. Proactive communication with your loan servicer is key to successfully navigating these challenges and maintaining a positive relationship during your career transition.

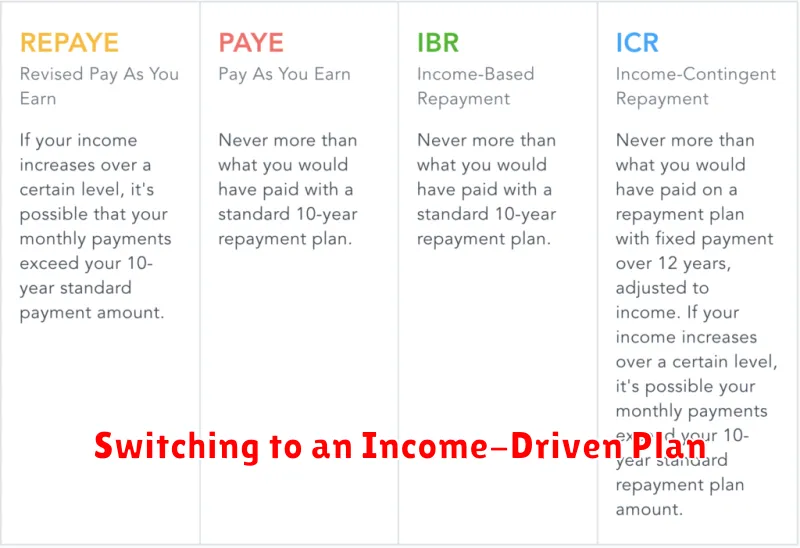

Switching to an Income-Driven Plan

A career change often brings financial uncertainty, and managing student loan debt can feel particularly overwhelming during this transition. One effective strategy to alleviate this burden is to switch to an income-driven repayment (IDR) plan. IDR plans link your monthly payments to your income and family size, offering potentially lower payments than standard repayment plans.

Several types of IDR plans exist, including Income-Based Repayment (IBR), Pay As You Earn (PAYE), and Revised Pay As You Earn (REPAYE). Each plan has specific eligibility requirements and payment calculation methods. It’s crucial to carefully compare these options to determine which plan best suits your individual financial situation.

Switching to an IDR plan can significantly reduce your monthly payments, freeing up more of your income to focus on your new career. This can provide crucial financial breathing room while you navigate the initial stages of your career transition, allowing you to concentrate on building your skills and experience without the added pressure of high student loan payments.

Important considerations when switching to an IDR plan include understanding the terms and conditions, such as potential forgiveness after a certain number of years and the accumulation of interest that may capitalize at the end of the repayment period. It is also important to accurately report your income annually to ensure your payments remain appropriate for your financial circumstances. Consulting with a financial advisor specializing in student loan debt can provide valuable guidance during this process.

Before making any changes to your repayment plan, it is strongly recommended to contact your loan servicer to understand the implications and complete the necessary application procedures. This will help ensure a smooth transition and minimize any potential complications.

Avoiding Missed Payments During Instability

A career change often involves a period of financial instability. Income may be reduced or temporarily nonexistent during the transition. This makes managing student loan payments a significant challenge. Proactive planning is crucial to avoid missed payments and the associated negative consequences, such as damage to your credit score and potential collection actions.

One of the most effective strategies is to explore deferment or forbearance options. These programs, offered by federal student loan providers, allow temporary suspension of payments or reduction in payment amounts. Eligibility requirements vary depending on the specific program and your circumstances. Carefully review the terms and conditions of any deferment or forbearance, as interest may still accrue during these periods, potentially increasing your overall loan balance.

Communicating with your loan servicer is paramount. Inform them proactively about your career change and the potential impact on your ability to make timely payments. Open communication can pave the way for customized solutions, such as temporary payment adjustments or enrollment in income-driven repayment plans. These plans tie your monthly payments to your income, making them more manageable during periods of financial uncertainty.

Consider creating a realistic budget that accounts for all income and expenses. Prioritize essential expenses, including housing, food, and transportation, while identifying areas where spending can be reduced. This careful budgeting can help free up funds to allocate towards student loan payments, even during times of lower income. Budgeting tools and apps can aid in this process.

Finally, explore alternative income sources during the transition period. This could involve freelancing, part-time employment, or tapping into savings. Supplementing your income even temporarily can help bridge the gap and avoid missed payments while you establish yourself in your new career.

How to Communicate With Your Loan Servicer

Maintaining open and consistent communication with your student loan servicer is crucial, especially during a career transition. Proactive communication can prevent misunderstandings and help you navigate potential challenges effectively.

Your first step should be to gather all relevant information. This includes your loan servicer’s contact information (phone number, mailing address, and online portal access), your loan account numbers, and a clear understanding of your current loan repayment plan.

When contacting your servicer, be prepared to explain your situation clearly and concisely. Clearly state that you’ve experienced a career change and outline how this impacts your ability to make your current payments. For instance, explain if you’ve experienced a reduction in income or are facing unemployment.

Consider exploring available options. Many servicers offer forbearance, deferment, or income-driven repayment plans. Be sure to ask about these options and their implications. Thoroughly understand the terms and conditions of each before making a decision. Inquire about any potential fees or penalties associated with modifying your payment plan.

Keep detailed records of all communication with your loan servicer. This includes dates, times, the method of contact (phone, email, mail), and a summary of the conversation or correspondence. This documentation can be invaluable in case of any future disputes or misunderstandings.

Remember to remain polite and professional throughout your interactions. A respectful approach can significantly improve your chances of finding a mutually agreeable solution. If you encounter difficulties or feel your concerns are not being adequately addressed, consider seeking assistance from a consumer credit counselor or financial advisor.

Rebuilding Your Repayment Schedule Post-Transition

A career change often necessitates a reassessment of your financial situation, and student loan repayment is a significant component of this. Your previous repayment plan, tailored to your former salary, may no longer be sustainable. The transition period, especially if it involves a temporary reduction in income, might leave you struggling to make timely payments.

Your first step should be to thoroughly evaluate your new financial landscape. This includes your current income, expenses, and any other debts you may have. A detailed budget will provide a clear picture of your disposable income and how much you can realistically allocate towards student loan payments.

Once you have a firm grasp of your finances, explore the various repayment options available to you. Depending on your loan type and servicer, you might be eligible for an income-driven repayment plan (IDR). IDRs adjust your monthly payments based on your income and family size, potentially lowering your payments during periods of lower income. Consider carefully the long-term implications of each plan, as some may result in higher total interest paid.

Communicating with your loan servicer is crucial. They can provide information on available repayment options, help you navigate the application process for IDRs, and potentially offer temporary forbearance or deferment if you’re experiencing significant financial hardship. Don’t hesitate to reach out; proactive communication can prevent delinquency and protect your credit score.

Finally, consider exploring additional income streams to supplement your current earnings. This might involve freelancing, part-time work, or selling unused assets. Even small increases in income can make a substantial difference in your ability to manage your student loan debt effectively while navigating your career transition.

{kind=link}