Student loan consolidation can seem like a simple solution to managing multiple student loan payments, but it’s crucial to understand the implications before making a decision. This comprehensive guide will equip you with the knowledge necessary to determine if consolidating your student loans is the right choice for your financial situation. We’ll delve into the pros and cons, exploring factors like interest rates, repayment plans, and the potential impact on your credit score. Understanding these aspects will empower you to make an informed decision that aligns with your long-term financial goals.

Before you rush into student loan refinancing or consolidation, it’s vital to carefully weigh the benefits and drawbacks. This includes analyzing your current loan terms, assessing potential changes to your monthly payments, and considering the long-term effects on your overall debt. We’ll provide clear explanations of the different types of consolidation programs available and guide you through the steps involved in the application process. This information will empower you to navigate the complexities of student loan consolidation and make a decision that best serves your financial well-being.

Difference Between Consolidation and Refinancing

While both consolidation and refinancing aim to simplify your student loan payments, they operate differently and have distinct implications. Understanding these differences is crucial before making a decision.

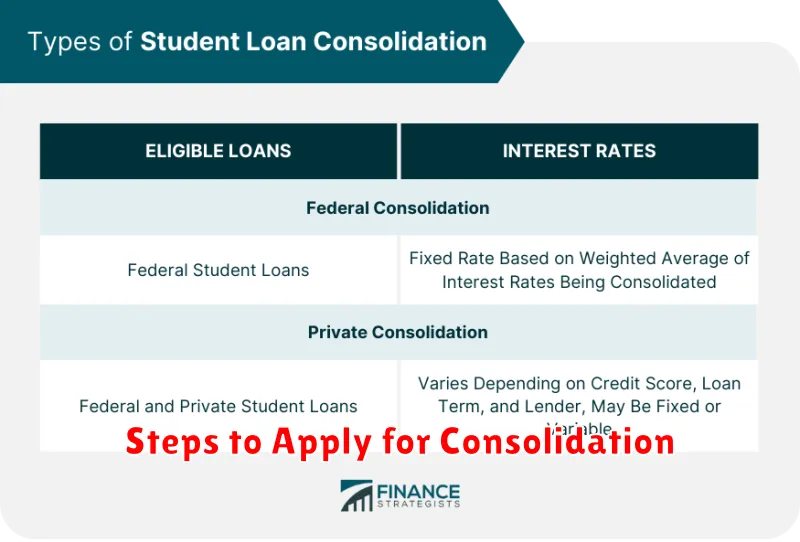

Consolidation involves combining multiple federal student loans into a single new federal loan. The interest rate on the new loan is a weighted average of the interest rates on your existing loans. This process is managed by the federal government through the Department of Education. Crucially, consolidation does not change your interest rate, although it can simplify repayment by combining multiple payments into one.

Refinancing, on the other hand, involves replacing your existing student loans – whether federal or private – with a new private loan from a lender, such as a bank. The new loan typically offers a lower interest rate than your existing loans, leading to potential savings over the life of the loan. However, refinancing federal student loans means losing access to federal repayment programs and benefits, such as income-driven repayment plans and deferment options. Refinancing also requires a credit check, and approval is not guaranteed.

In short, consolidation simplifies your payments by combining loans but doesn’t alter your interest rate, while refinancing offers potential for lower interest rates but involves a risk of losing federal benefits and requires a good credit standing. The best option depends on your individual financial situation and priorities.

Loans Eligible for Federal Consolidation

Federal student loan consolidation simplifies your repayment by combining multiple federal student loans into a single loan with one monthly payment. However, not all federal loans are eligible for consolidation. Understanding which loans qualify is crucial before proceeding.

Generally, the following types of federal student loans are eligible for consolidation: Direct Subsidized Loans, Direct Unsubsidized Loans, Direct PLUS Loans (for graduate or professional students and parents), Federal Stafford Loans (Subsidized and Unsubsidized), Federal Consolidation Loans (you can consolidate existing consolidation loans), and Federal Perkins Loans.

It’s important to note that private student loans are not eligible for federal consolidation programs. These must be managed separately. Similarly, loans obtained through other federal programs, such as those for vocational rehabilitation, may not qualify. Reviewing your loan documents or contacting your loan servicer is crucial for confirming which loans are eligible.

Consolidating your loans may affect your repayment terms, including the interest rate. The interest rate on a consolidated loan is typically a weighted average of the interest rates on your existing loans, rounded up to the nearest one-eighth of one percent. This new rate will be fixed for the life of the loan. Understanding the impact on your interest rate is a key consideration.

Before you consolidate, consider the implications for potential benefits, such as loan forgiveness programs. Some programs, like those based on public service, may have eligibility requirements affected by consolidation. Carefully weigh the pros and cons for your specific situation.

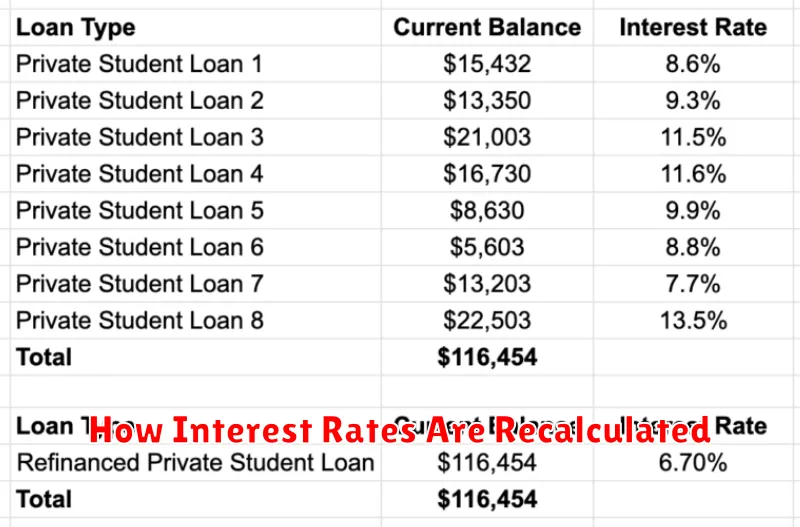

How Interest Rates Are Recalculated

When you consolidate your student loans, your interest rate is recalculated. This new rate is a weighted average of the interest rates on your existing loans. The weight given to each loan’s interest rate is determined by its principal balance; loans with larger balances will have a greater influence on the final rate.

The process isn’t simply averaging the rates. Instead, a weighted average is calculated. This considers the outstanding balance of each loan. For example, if one loan has a higher balance than others, its interest rate will have a proportionally greater impact on the new, consolidated rate.

The type of consolidation also plays a role. Federal Direct Consolidation loans typically use a fixed interest rate based on the weighted average of your previous loans’ rates, rounded up to the nearest one-eighth of a percent. The rate is then fixed for the life of the loan, providing predictability.

It’s crucial to understand that while consolidation simplifies payments, it doesn’t necessarily lower your overall interest rate. Your new rate may be higher or lower than your highest existing rate, depending on the balance and rates of your individual loans. It is therefore recommended to carefully compare the potential total interest paid under different consolidation options.

Your lender will provide you with a clear explanation of how your new interest rate was calculated before you finalize the consolidation. Reviewing this information is vital to ensure you understand the implications of the process on your overall loan repayment.

Pros: Simpler Payments, Extended Terms

One of the most appealing aspects of student loan consolidation is the simplification of your payment process. Instead of juggling multiple monthly payments to various lenders, you’ll have a single, consolidated payment. This streamlined approach can significantly reduce administrative hassle and improve organization.

Another key advantage is the potential for an extended repayment term. Consolidating your loans might allow you to stretch your repayment schedule over a longer period. This, in turn, lowers your monthly payment amount, making it more manageable in the short term. However, it’s crucial to remember that extending your repayment term will ultimately increase the total interest you pay over the life of the loan. Carefully weigh the benefits of a lower monthly payment against the increased long-term cost.

Furthermore, consolidation can offer improved flexibility in your repayment plan. Some consolidation programs provide options like income-driven repayment plans, which adjust your monthly payment based on your income and family size. This can be particularly beneficial during periods of financial hardship.

Finally, consolidating your loans can potentially lead to a lower interest rate, although this isn’t guaranteed. If you qualify for a lower rate, it could result in substantial savings over the repayment period. However, be sure to compare the interest rates offered by various consolidation programs before making a decision to ensure you are securing the best possible rate.

Cons: Longer Debt, Loss of Certain Benefits

One of the most significant drawbacks of student loan consolidation is the potential for a longer repayment period. While a lower monthly payment might seem appealing, extending the loan term means you’ll ultimately pay more in interest over the life of the loan. This increased interest expense can significantly outweigh any short-term savings from a reduced monthly payment.

Furthermore, consolidating your loans can lead to the loss of certain benefits associated with your individual loans. For instance, you might forfeit access to income-driven repayment plans, loan forgiveness programs (like those for public service employees), or other advantageous repayment options specific to certain loan types. It’s crucial to carefully weigh the potential loss of these benefits against the advantages of consolidation before making a decision. Carefully review the terms of your existing loans and the terms of the consolidated loan to fully understand the implications.

Another potential disadvantage is the impact on your credit score. While consolidation itself doesn’t directly hurt your credit, the lengthier repayment period could negatively affect your credit utilization ratio if not managed properly. Additionally, the application process for consolidation may result in a temporary, minor dip in your credit score, depending on the lender’s policies.

Finally, consolidating federal student loans into a private loan will result in the loss of all federal protections. This includes the ability to defer or forbear payments under certain circumstances and the access to various income-driven repayment plans.

Steps to Apply for Consolidation

The process of applying for student loan consolidation involves several key steps. First, you need to gather all the necessary information regarding your existing student loans. This includes loan servicers, account numbers, and outstanding balances. Thorough record-keeping is crucial for a smooth application.

Next, you should carefully consider which consolidation program best suits your needs. The federal government offers a Direct Consolidation Loan program, while private lenders also provide consolidation options. Understanding the terms and conditions of each program is paramount before making a decision. Factors such as interest rates, fees, and repayment terms should be carefully weighed.

Once you’ve chosen a program, complete the application form accurately and thoroughly. Ensure all the information provided is correct to prevent delays or rejections. This typically involves providing personal details, loan information, and possibly additional documentation as requested.

After submitting your application, you’ll need to allow processing time. The timeframe for approval can vary depending on the lender and the complexity of your application. Regularly check the status of your application through the lender’s online portal or by contacting customer support.

Finally, once your application is approved, you’ll receive your new consolidated loan information. This includes your new loan servicer, repayment schedule, and interest rate. It’s vital to understand the terms of your new loan and keep track of your repayment progress.

{kind=link}