Understanding your credit limit is crucial for effective credit card management. This seemingly simple number represents the maximum amount of money a lender allows you to borrow on your credit card at any given time. Knowing your credit limit helps you avoid high-interest charges and maintain a healthy credit score. This article will delve into the intricacies of credit limits, explaining what they are, how they’re determined, and how to improve yours.

Many factors influence your credit limit, including your credit history, income, and the type of credit card you apply for. We’ll explore how your payment history, debt-to-income ratio, and even your credit utilization play a role in the credit limit you’re offered. Learn how to navigate the process of obtaining a favorable credit limit and make informed decisions about your credit card usage to optimize your financial health. This guide offers a clear and concise overview of this critical aspect of personal finance.

Definition of Credit Limit

A credit limit is the maximum amount of money a lender allows a borrower to access on a line of credit, such as a credit card or loan. It represents the upper bound of the credit extended to the borrower.

This limit is pre-determined by the lender based on several factors, and exceeding it can result in penalties, including high interest charges and damage to the borrower’s credit score. It’s crucial to understand and manage one’s credit limit responsibly to avoid financial difficulties.

The credit limit acts as a safety net, preventing overspending and ensuring the borrower’s ability to repay the debt within a manageable timeframe. It’s a key element in determining a borrower’s creditworthiness and their overall financial health.

Understanding your credit limit is essential for budgeting and financial planning. Staying within this limit is vital for maintaining a positive credit history and accessing better credit opportunities in the future. Responsible credit usage is paramount for long-term financial well-being.

Factors Lenders Consider for Your Limit

Several key factors influence the credit limit a lender offers. Understanding these factors can help you improve your chances of securing a higher limit.

Credit score is paramount. A higher credit score, demonstrating responsible credit management, typically results in a higher credit limit. Lenders view a strong score as a reduced risk of default.

Your credit history is carefully examined. Length of credit history, types of credit accounts (credit cards, loans, etc.), and payment history all play a crucial role. A longer history with consistent on-time payments is generally favorable.

Income and debt levels are also significant. Lenders assess your ability to repay the debt by analyzing your income against your existing debts. A higher income relative to your debt suggests a greater capacity to manage additional credit.

The type of credit card or loan you are applying for matters. Different lenders have different criteria, and secured credit cards often have lower limits than unsecured cards.

Your application information is scrutinized. Accuracy and completeness are vital. Inaccurate or incomplete information can negatively impact your chances of obtaining a favorable credit limit.

Collateral, in the case of secured credit cards or loans, influences the limit significantly. The value of the collateral acts as a safeguard for the lender, often leading to higher limits.

Finally, the lender’s own policies and risk appetite play a role. Different lenders have varying approval criteria, and their internal risk assessments will influence the limits offered.

How It Affects Your Spending and Score

Your credit limit significantly impacts your spending habits. A higher limit can create a false sense of financial security, leading to increased spending and potential overspending. Conversely, a lower limit may restrict your spending, encouraging more responsible financial behavior and preventing debt accumulation.

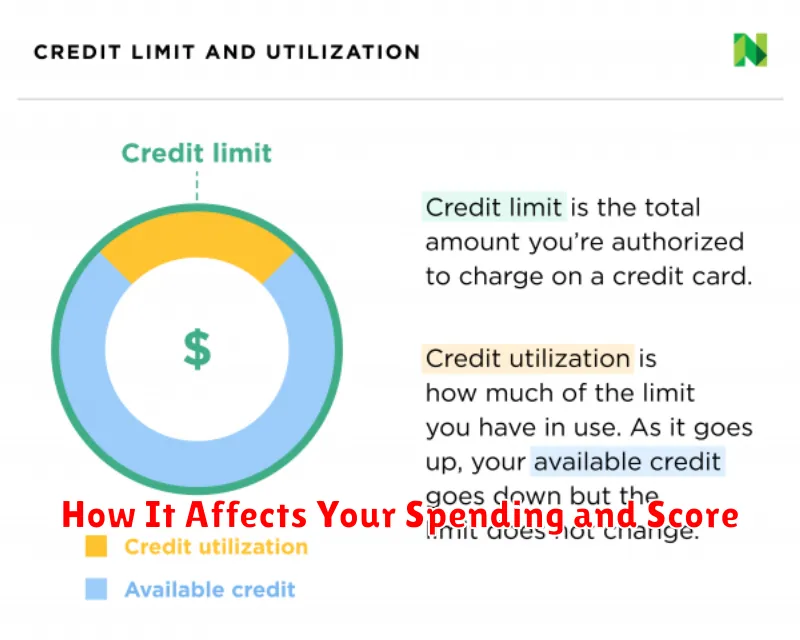

Your credit limit also plays a crucial role in your credit score. A key factor in credit scoring is your credit utilization ratio, which is the percentage of your available credit that you’re currently using. Maintaining a low credit utilization ratio (generally below 30%) is vital for a good credit score. A high credit utilization ratio, even if you pay your bills on time, can negatively impact your score, signaling to lenders that you may be overextended financially.

For example, if you have a credit limit of $10,000 and carry a balance of $8,000, your credit utilization is 80%. This is considered high and will likely lower your credit score. However, if you have the same $10,000 limit but only use $2,000, your utilization is only 20%, which is considered healthy and beneficial for your score.

Therefore, understanding your credit limit and managing your spending accordingly is essential for maintaining a healthy financial life and a strong credit score. Responsible credit card use involves spending within your means and keeping your credit utilization ratio low.

Can You Request a Higher Limit?

Yes, you can typically request a higher credit limit from your credit card issuer. This process is often referred to as a credit limit increase.

The success of your request depends on several factors. Credit card companies assess your creditworthiness before approving an increase. They will review your credit report, looking at your credit score, payment history, and overall credit utilization. A strong credit history, demonstrating responsible credit management, significantly increases your chances of approval.

The process usually involves contacting your credit card issuer, either through their website or by phone. They may request additional financial information to support your request, such as proof of income or employment. Be prepared to provide this documentation promptly to expedite the process.

It is important to understand that not all requests for credit limit increases are approved. The issuer may deny your request if they perceive an increased risk based on your financial circumstances. If your request is denied, inquire about the reason for the denial and steps you can take to improve your chances of approval in the future.

It’s generally advisable to request a credit limit increase gradually rather than attempting a large increase all at once. Smaller, incremental increases can demonstrate responsible credit behavior and improve your chances of success over time.

When a Lower Limit Can Be a Good Thing

While a high credit limit might seem desirable, a lower limit can actually be beneficial in certain situations. This is particularly true for individuals working on improving their credit score or managing their spending habits.

A lower limit can help prevent overspending. With less readily available credit, you’re less likely to make impulse purchases or rack up significant debt. This is especially crucial for those with a history of overspending or difficulty managing their finances.

For those rebuilding their credit, a lower limit can lead to a lower credit utilization ratio. This ratio, which compares your credit card balance to your credit limit, is a significant factor in your credit score. Keeping your utilization ratio low (ideally below 30%) is key to demonstrating responsible credit management, and a lower limit makes this significantly easier to achieve.

Furthermore, a lower limit can be a good starting point for those newly establishing credit. Credit card issuers may offer a lower limit to new applicants as a way to assess creditworthiness and responsible borrowing habits before increasing the limit in the future.

Finally, a lower limit can mean lower interest charges. If you carry a balance, a lower limit translates to a smaller balance on which interest accrues, saving you money in the long run. However, this only applies if you are carrying a balance, and it’s crucial to try and pay your balance in full each month to avoid interest altogether.

What Happens if You Go Over the Limit

Exceeding your credit limit, also known as going over your credit limit or exceeding your credit card limit, can trigger several consequences, impacting both your finances and credit score.

One of the most immediate consequences is the imposition of over-limit fees. These fees can range significantly depending on your credit card issuer, and they can add up quickly. The exact amount of the fee is typically outlined in your credit card agreement.

Beyond the fees, your interest rate may increase. Many credit card companies charge a higher interest rate on balances that exceed the credit limit. This higher interest rate applies to the entire outstanding balance, not just the amount exceeding the limit, potentially increasing your monthly payments significantly.

Furthermore, going over your credit limit can negatively impact your credit score. Credit bureaus view exceeding your credit limit as a sign of poor financial management. This can make it more difficult to obtain credit in the future, and it may also lead to higher interest rates on loans and other forms of credit. It can significantly reduce your creditworthiness.

Your credit card company may also deny further transactions until your balance falls below the credit limit. This can be particularly disruptive if you rely on your credit card for regular expenses. In some cases, your card may be suspended entirely.

Finally, some credit card companies may choose to close your account altogether if you consistently exceed your credit limit. This can severely limit your access to credit and leave a negative mark on your credit report.

{kind=link}